How to Nominate Beneficiaries in Indian Mutual Funds and Update Details

When you invest in mutual funds in India, your money grows over time-but what happens to those investments if something unexpected happens to you? That’s where naming a beneficiary comes in. It’s not just paperwork. It’s peace of mind. Many investors in India skip this step, thinking it’s optional or too complicated. But if you die without a nominee, your mutual fund units go into legal limbo. Your family might face delays, paperwork nightmares, or even court battles just to access what’s theirs. The good news? Setting up or updating a nominee is simple, fast, and free.

Why Nominees Matter in Mutual Funds

Indian mutual funds are regulated by SEBI, and under their rules, every folio must have at least one nominee. This isn’t a suggestion-it’s mandatory. Without a nominee, the fund house can’t transfer your holdings after your death. Even if you have a will, the process becomes slower and more expensive. Banks and demat accounts also require nominees, but mutual funds are different. They don’t automatically follow your will. The nominee gets the units directly, bypassing probate.

Let’s say you invested ₹5 lakh in a growth fund over five years. You didn’t name anyone. Now, you pass away suddenly. Your spouse tries to claim the amount. The AMC (Asset Management Company) asks for a succession certificate, death certificate, proof of relationship, and more. It can take six months to a year. If you had named your spouse as nominee, they’d get the money in under 15 days with just two documents: their ID and your death certificate.

Who Can Be a Nominee?

Not everyone qualifies. SEBI allows only certain people to be nominees in mutual funds:

- Spouse

- Children (including adopted)

- Parents

- Legal heir (if no other nominee is named)

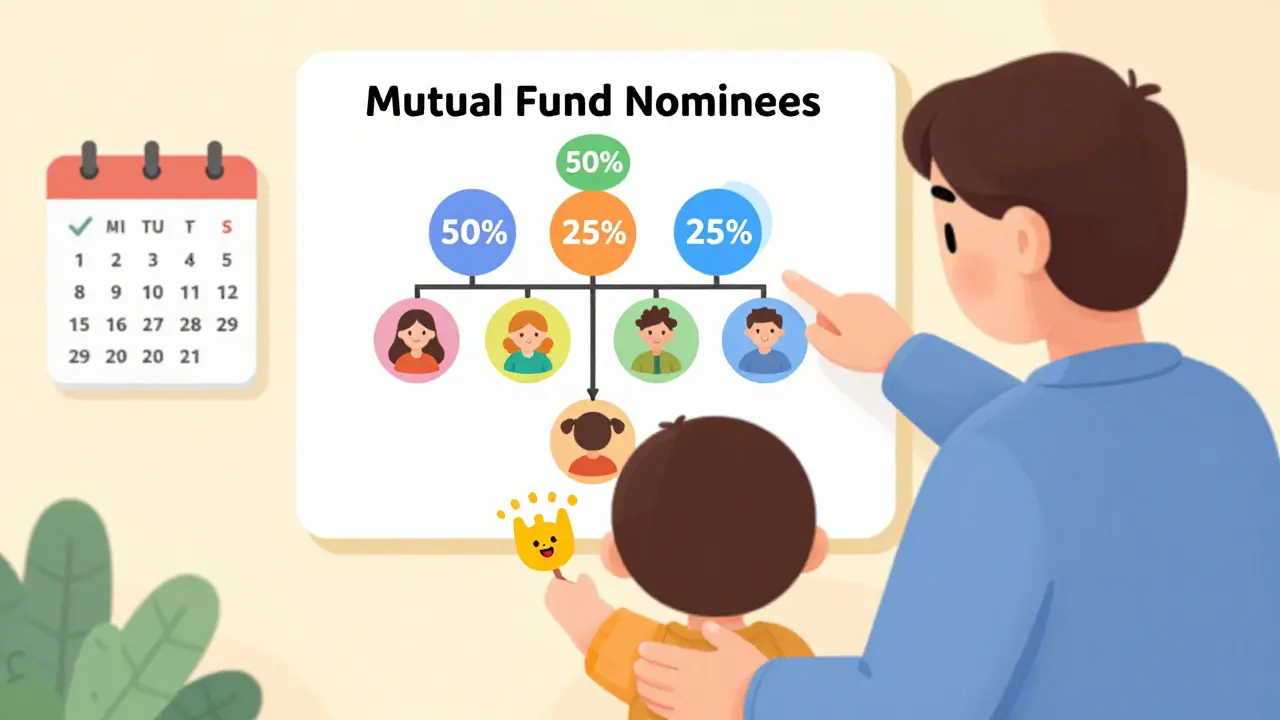

You cannot name a friend, neighbor, charity, or trust as a nominee. The nominee must be a natural person-no companies or organizations. You can name up to three nominees, and you must specify the percentage each gets. For example: 50% to your spouse, 25% to each child. If you don’t specify percentages, it’s assumed to be equal.

Minors can be nominees too-but you must also name a guardian who will manage the funds until the child turns 18. That guardian can’t be the same person as the nominee unless they’re the parent.

How to Add a Nominee When You First Invest

If you’re just starting out, adding a nominee is built into the process. When you open a mutual fund account-whether through an app like Zerodha Coin, Groww, or directly with a fund house like HDFC or ICICI Prudential-you’ll be asked to fill out a nomination form. This happens during KYC verification.

Here’s what you’ll need:

- Your PAN card

- Proof of address (Aadhaar, driver’s license, utility bill)

- Name, date of birth, and relationship of the nominee(s)

- Photograph of the nominee (if they’re a minor, the guardian’s photo)

Most platforms now let you do this digitally. You upload a photo of your nominee’s ID, enter their details, and sign electronically. No physical form needed. Once submitted, the nomination is active within 24-48 hours.

How to Update a Nominee Later

Life changes. You get married. Your child turns 18. Your parent passes away. You need to update your nominee. The process is just as easy.

Step 1: Log in to your mutual fund platform. This could be your distributor’s app, the fund house’s website, or CAMS/NSDL’s portal if you hold funds through them.

Step 2: Go to your profile or account settings. Look for “Nomination” or “Beneficiary Details.”

Step 3: Click “Update Nominee.” You’ll see your current nominee(s). You can add, remove, or change percentages.

Step 4: Enter new nominee details. You’ll need their full name, date of birth, PAN (if they have one), and relationship to you. Upload a clear photo of their ID.

Step 5: Submit and sign digitally. You’ll get an OTP on your registered mobile. Confirm it. Done.

Most platforms process updates within 2 business days. You’ll get an email or SMS confirmation. Keep it.

What If You Have Multiple Folios?

If you invest through different fund houses-say, SBI Mutual Fund, Axis Mutual Fund, and Kotak-you’ll have separate folios. Each folio needs its own nomination. There’s no central database. You can’t set one nominee for all your funds. You must update each one individually.

Tip: Keep a simple spreadsheet. List each fund house, folio number, current nominee, and date last updated. Update it every time you change something. It takes five minutes once a year.

What Happens If You Don’t Update After Marriage or Divorce?

This is where things get messy. Let’s say you nominated your parents before you got married. You never updated it. After you pass away, your spouse finds out they’re not the nominee. Legally, your parents are entitled to the money-even if you left a will saying it should go to your wife.

SEBI doesn’t override nominations with wills. The nominee gets the assets first. Your spouse can still claim a share through legal inheritance, but they’ll need to go to court. That costs money, time, and emotional energy.

Same goes for divorce. If you divorced but didn’t remove your ex-spouse as nominee, they still get the money. Courts won’t automatically cancel the nomination. You have to do it yourself.

Common Mistakes People Make

Here are the top three errors-and how to avoid them:

- Mistake: Naming a minor without a guardian. Fix: Always name a guardian when the nominee is under 18. The guardian must be an adult with a valid ID.

- Mistake: Using nicknames or initials. Fix: Use full legal names exactly as they appear on ID cards. “Raj” won’t work. “Rajesh Kumar Sharma” will.

- Mistake: Assuming your will covers everything. Fix: Your will is important-but it doesn’t override your mutual fund nominee. Both should align.

Another big one: people forget to update nominees after changing their own name. If you changed your name after marriage, your folio must reflect your new name. Otherwise, the system won’t match your ID with your nominee details. Update your name with the fund house first, then your nominee.

What About Joint Accounts?

If you hold mutual funds jointly-with your spouse, for example-the rules change slightly. The nominee only comes into play if both holders die. If one dies, the units automatically transfer to the surviving holder. No nominee needed at that point.

But if you both pass away, the nominee gets the entire holding. So even in joint accounts, you still need a nominee. Don’t skip it.

How to Check Your Current Nominee

Not sure who’s listed? Here’s how to find out:

- Log in to your fund house’s website or app

- Go to “Portfolio” or “Holdings”

- Click on any fund and look for “Nominee Details”

- Or check your latest statement-it’s usually printed at the bottom

- If you use CAMS or KFinTech as registrar, log in to their portal: camsonline.com or kfintech.com (you’ll need your folio number)

If you don’t remember your folio number, call the AMC’s customer care. They can look it up using your PAN.

What If You Lose Your Nominee Details?

If you’ve lost all records and can’t log in anywhere, send a written request to the fund house. Include:

- Your full name

- Your PAN

- Your registered mobile number

- Your address

- A copy of your ID

They’ll mail you a copy of your nominee details within 7-10 working days. No fee.

Do Nominees Pay Tax?

No. The nominee receives the mutual fund units as they are. If they sell them later, capital gains tax applies based on how long you held them. If you held for more than one year (equity funds), the gain is taxed at 10% over ₹1 lakh. If less than a year, it’s taxed at 15%. The nominee inherits your holding period. They don’t pay tax just for receiving the units.

It’s not inheritance tax. India doesn’t have that. So the transfer is tax-free. Only future sales trigger tax.

Final Checklist Before You Close This Page

Take two minutes now. Do this:

- Log in to your top mutual fund account

- Check your nominee

- If it’s outdated, update it today

- Write down your folio numbers and nominees in one place

- Share the location of this list with a trusted family member

That’s it. No lawyer needed. No forms to print. No waiting in lines. Just a few clicks-and you’ve protected your family’s future.

Can I change my nominee anytime?

Yes. You can update your nominee anytime, as many times as you want. There’s no limit. You don’t need to wait for a specific date or pay any fee. Just log in to your fund house’s platform and make the change.

What if my nominee dies before me?

If your nominee passes away before you, their share becomes invalid. You need to update your nomination to name someone else. If you don’t, and you pass away, the fund house will treat the deceased nominee’s share as unclaimed. It will then be distributed to your legal heirs through probate, which delays the process.

Can I name my pet as a nominee?

No. Only natural persons-humans-are allowed as nominees. You cannot name animals, trusts, charities, or companies. If you want to leave money for your pet, you’ll need to create a will and appoint a trustee to manage it.

Do I need to inform my nominee?

You’re not legally required to tell them. But it’s strongly advised. If your nominee doesn’t know they’re named, they won’t know to claim the funds after your death. This can cause unnecessary delays. Share your folio details and nominee info with someone you trust.

Can I have different nominees for different funds?

Yes. Each mutual fund folio is independent. You can name your spouse as nominee for your HDFC fund, your child for your ICICI fund, and your parent for your Axis fund. There’s no rule that forces you to use the same nominee across all accounts.