Section 80C Lock-In and Liquidity Rules in India: A Practical Guide for Investors

You’ve just hit your annual salary cap. You’re looking at the Section 80C is a provision in the Indian Income Tax Act that allows individuals to claim deductions on specific investments and expenses up to ₹1.5 lakh per financial year. limit of ₹1.5 lakh. Your goal? Save taxes. But here’s the catch: most of these instruments come with strings attached. Specifically, they lock your money away for years. If you need cash for a medical emergency or an unexpected opportunity, can you get it? Or will you be stuck paying heavy penalties?

The answer isn’t a simple yes or no. It depends entirely on which instrument you chose. Some offer partial liquidity with tax hits; others are completely rigid until maturity. Understanding the difference between lock-in periods are mandatory holding durations required by law or contract before an investor can withdraw funds from certain tax-saving instruments. and actual liquidity is crucial. This guide breaks down exactly what happens when you try to access your money early, who pays the price, and how to structure your portfolio so you aren’t trapped.

The Core Concept: What Actually Gets Locked In?

When people talk about Section 80C, they usually mean the deduction itself. But the deduction is just the benefit. The cost is the restriction on access. Not all 80C instruments have the same rules. Some have strict legal lock-ins enforced by the government. Others have contractual lock-ins set by the fund house or bank. And some have no lock-in at all but lose their tax benefit if withdrawn too soon.

It is vital to distinguish between these three types because they dictate your exit strategy:

- Statutory Lock-In: These are mandated by law (like Provident Funds). You cannot touch the money under any circumstances until the time is up, except in very specific life events like marriage or higher education for children.

- Contractual Lock-In: These are set by the provider (like Equity Linked Savings Schemes - ELSS). You can often redeem units after the minimum period, but doing so might trigger tax consequences or loss of benefits.

- Tax-Benefit Conditionality: Instruments like PPF (Public Provident Fund) allow partial withdrawals after a certain age, but only if you’ve held the account long enough. If you close it early, you lose the interest and potentially face tax adjustments.

Knowing which bucket your investment falls into saves you from panic when cash flow tightens. Let’s look at the big players one by one.

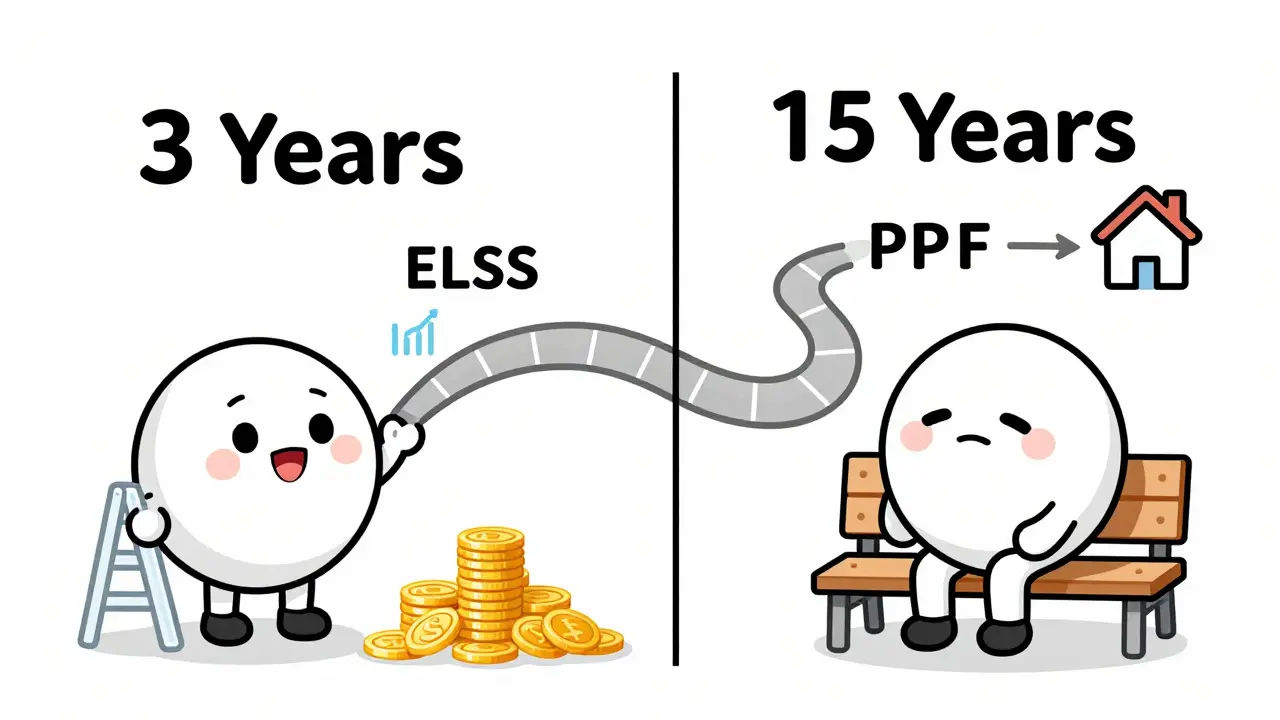

ELSS: The Shortest Lock-In, But With Caveats

If liquidity is your top priority among tax-saving tools, Equity Linked Savings Scheme (ELSS) is a type of mutual fund in India that invests primarily in equities and offers tax benefits under Section 80C with a mandatory lock-in period of 3 years. is likely your best bet. It has the shortest statutory lock-in period of just three years. That means once you buy units, they are frozen for 36 months. After that, you can sell them anytime.

However, "liquid" doesn’t mean "free." Here is what you need to watch out for:

- Market Risk: Since ELSS is equity-heavy, the value of your investment fluctuates. If the market crashes right after your lock-in ends, you might withdraw less than you invested. Liquidity exists, but capital preservation is not guaranteed.

- Long-Term Capital Gains (LTCG): If you make a profit and sell after three years, you pay 10% LTCG tax on gains exceeding ₹1 lakh in a financial year. This is separate from the income tax you saved via 80C.

- No Partial Withdrawals During Lock-In: You cannot pull out half your money in year two. The entire amount sits there. If you need ₹50,000 for an emergency but have ₹1.5 lakh locked in ELSS, you are out of luck until day 730.

For many investors, this three-year window is acceptable. It’s short enough to plan around, yet long enough to smooth out some market volatility. But if you think you might need that cash in 18 months, ELSS is not the right vehicle.

PPF and Sukanya Samriddhi: The Long Haul

On the other end of the spectrum are Public Provident Fund (PPF) is a government-backed savings scheme in India with a 15-year tenure, offering tax-free returns and partial withdrawal facilities after seven years. and Sukanya Samriddhi Yojana (SSY) is a government-sponsored savings scheme for the girl child in India, offering high interest rates and full tax exemption on maturity.. These are designed for retirement or long-term goals, not short-term flexibility.

PPF has a 15-year lock-in. However, it does offer a middle ground. From the seventh financial year onwards, you can make partial withdrawals. You can take out up to 50% of the balance at the end of the fourth year preceding the current year or the end of the third year preceding the year of withdrawal, whichever is lower. This is useful for large expenses like buying a home or funding education. But remember, you can only do this once a year. And if you close the account before 15 years, you lose the compounding advantage significantly.

Sukanya Samriddhi is even stricter. It locks in until the girl child turns 21. Partial withdrawals are allowed only for her higher education or marriage after she turns 18. There is almost no liquidity for the parent during the accumulation phase. This makes SSY ideal if you have a daughter and want to force-save for her future, but terrible if you need personal access to those funds.

Life Insurance Premiums: Surrender Value vs. Cash Flow

Many people still use traditional endowment plans or whole life policies to save tax under 80C. The premium payments are deductible. But what if you stop paying? Or what if you need the money back?

Here, the concept is surrender value, not liquidity. If you surrender the policy before maturity, you get back a percentage of the premiums paid, minus administrative charges and penalties. In the early years, this surrender value can be negligible. You might have paid ₹1 lakh in premiums but only get back ₹20,000 if you quit in year two. This is a massive loss of capital.

Furthermore, if you surrender the policy, you may have to reverse the tax benefits claimed in previous years. The Income Tax Department treats this as taxable income in the year of surrender. So, not only do you lose money, but you also owe more tax. Term insurance, by contrast, has no cash value and thus no liquidity issue-it’s pure protection. Endowment plans are illiquid traps unless you hold them to maturity.

Tax-Saving Fixed Deposits: The Middle Ground

Tax-Saving Fixed Deposits (FDs) are bank deposits with a mandatory 5-year lock-in period that offer tax deductions under Section 80C and fixed interest rates. offer a predictable return with a five-year lock-in. Unlike ELSS, there is no market risk. Unlike PPF, the tenure is shorter. But the liquidity is zero during those five years. You cannot break the FD without severe penalties, and often, banks simply don’t allow premature closure for tax-saving FDs at all.

Some banks may allow it, but they will deduct the interest earned and charge a penalty. More importantly, the tax benefit you claimed in earlier years might become taxable. The rule is complex: if you break the FD, the interest accrued becomes taxable in the year of withdrawal, and you may have to adjust the 80C deduction in your ITR. It’s messy and generally discouraged.

| Instrument | Lock-In Period | Liquidity Options | Penalty for Early Exit |

|---|---|---|---|

| ELSS | 3 Years | Full redemption after 3 years | None (but market risk applies) |

| Tax-Saving FD | 5 Years | Usually none | Loss of interest + potential tax reversal |

| PPF | 15 Years | Partial withdrawal from Year 7 | Reduced interest rate if closed early |

| Endowment Policy | Maturity Date | Surrender value (low in early years) | High capital loss + tax liability |

| NPS (Tier I) | Retirement Age | Limited loans against corpus | Not applicable (illiquid by design) |

National Pension System: Retirement Only

The National Pension System (NPS) is a voluntary, contributory pension scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA) in India. Tier I account is strictly for retirement. You cannot withdraw anything until you turn 60. At that point, 60% of the corpus can be withdrawn tax-free, and 40% must be used to buy an annuity. There is virtually no liquidity. The only exception is if you face a critical illness or unemployment for over a year, but even then, the process is bureaucratic and limited. NPS is not for short-term tax planning; it’s for old-age security.

Strategies to Maintain Liquidity While Saving Tax

So, how do you avoid being stranded without cash? You diversify your 80C allocation based on your cash flow needs. Don’t put all ₹1.5 lakh into one bucket.

Consider this approach:

- Emergency Buffer First: Before investing in any 80C instrument, ensure you have 3-6 months of expenses in a regular savings account or liquid fund. Do not mix emergency funds with tax-saving investments.

- Layer Your Investments: Put the amount you won’t need for 3+ years into ELSS. Put the amount you won’t need for 5+ years into Tax-Saving FDs. Put the long-term retirement money into PPF or NPS.

- Use Non-Lock-In 80C Options: Remember, 80C also covers principal repayment of home loans, tuition fees for two children, and health insurance premiums. These don’t have lock-ins in the same way. Paying off a mortgage reduces debt and frees up future cash flow, which is a form of liquidity.

- Review Annually: Life changes. Marriage, kids, job switches. Reassess your 80C mix every year. If you expect a large expense in two years, shift that portion from ELSS to a regular mutual fund (no lock-in) and use other 80C avenues like health insurance to cover the tax deduction.

The key is intentionality. Don’t just chase the highest return. Chase the right balance of safety, growth, and access.

Common Pitfalls to Avoid

Many investors make the mistake of assuming that because they saved tax, the money is "theirs" to spend later. It’s not. The tax department views premature withdrawals as a reversal of privilege. Be wary of:

- Ignoring Inflation: Locking money for 15 years in PPF sounds safe, but if inflation averages 6%, your purchasing power drops. Ensure your overall portfolio includes growth assets outside of 80C.

- Overlooking Exit Loads: Some ELSS funds charge exit loads if redeemed within the lock-in period (though rare due to statutory rules), or if redeemed shortly after. Check the scheme information document.

- Tax Surprises: Always calculate the net return after accounting for potential LTCG or reversal of benefits. A 9% return that turns into 6% after taxes and penalties is worse than a transparent 7% elsewhere.

Finally, consult a certified financial planner who understands both tax laws and asset allocation. Generic advice often fails because everyone’s liquidity needs are different.

Can I withdraw money from ELSS before 3 years?

No, you cannot withdraw money from an Equity Linked Savings Scheme (ELSS) before the mandatory 3-year lock-in period expires. Each unit purchased has its own individual lock-in date. Attempting to redeem early will result in rejection by the registrar.

What happens if I break my Tax-Saving Fixed Deposit?

Most banks do not allow premature closure of tax-saving FDs. If they do, you will likely lose the interest earned, face a penalty, and may have to reverse the tax benefits claimed in previous years, making it financially disadvantageous.

When can I withdraw from PPF?

You can make partial withdrawals from a Public Provident Fund (PPF) account starting from the beginning of the 7th financial year. You can withdraw up to 50% of the balance at the end of the 4th year preceding the current year or the 3rd year preceding the year of withdrawal, whichever is lower. Full withdrawal is allowed only after 15 years.

Is there any liquidity option in NPS Tier I?

NPS Tier I is highly illiquid and meant for retirement. Withdrawals are generally prohibited until age 60. Exceptions exist for critical illnesses or unemployment exceeding one year, but these require documentation and approval from the Pension Fund Regulatory and Development Authority (PFRDA).

Do I have to pay tax if I withdraw from ELSS after 3 years?

Yes, if you make a profit. Any capital gain exceeding ₹1 lakh in a financial year from selling ELSS units after 3 years is subject to a 10% Long-Term Capital Gains (LTCG) tax. Losses are not taxed.

Can I use Sukanya Samriddhi funds for my own expenses?

No. Sukanya Samriddhi Yojana funds are strictly for the benefit of the girl child. Partial withdrawals are permitted only for her higher education or marriage after she turns 18. Parents cannot access these funds for personal use.