How to Open an NPS Account in India and Start Contributing for Retirement

Opening an NPS account in India is one of the most straightforward ways to build a secure retirement fund-especially if you’re self-employed, a freelancer, or just want more control over your savings than a traditional pension offers. The National Pension System (NPS) is backed by the Indian government and regulated by PFRDA, making it one of the safest and most tax-efficient retirement schemes available today. Unlike fixed deposits or insurance policies, NPS gives you direct control over how your money is invested, with options to choose between equity, corporate bonds, and government securities.

What Is NPS and Why Should You Care?

NPS stands for National Pension System. It was launched in 2004 for government employees and opened to all Indian citizens in 2009. Since then, over 120 million accounts have been opened, with more than 80% of them being from the unorganized sector-people who don’t get employer-sponsored pensions.

Here’s the catch: NPS isn’t just another savings account. It’s designed to turn your monthly contributions into a lifelong income stream after age 60. At retirement, you can withdraw up to 60% of your corpus as a lump sum (tax-free if you meet the conditions), and the remaining 40% must be used to buy an annuity that pays you monthly for life. That’s the core structure-no guessing, no loopholes.

What makes NPS stand out? Three things: low fees, government backing, and tax breaks. The annual fund management charge is just 0.0009% of your balance-far lower than mutual funds or ULIPs. Plus, you can claim deductions under Section 80C (up to ₹1.5 lakh) and an extra ₹50,000 under Section 80CCD(1B), which no other investment offers.

Two Types of NPS Accounts: Tier I and Tier II

Before you sign up, you need to pick your account type. There are two: Tier I and Tier II.

- Tier I is mandatory for retirement savings. You can’t withdraw the money before 60, except in rare cases like critical illness, higher education, or buying a home. Contributions here qualify for tax deductions.

- Tier II is flexible. Think of it as a voluntary savings account. You can deposit and withdraw anytime, but there’s no tax benefit. It’s great for short-term goals or as a buffer while you’re building your Tier I corpus.

Most people start with Tier I. You can open Tier II later if you need more flexibility. But you can’t open Tier II without having a Tier I account first.

Who Can Open an NPS Account?

Any Indian citizen aged between 18 and 70 can open an NPS account. Non-resident Indians (NRIs) can also join, but they can’t contribute after turning 60, and withdrawals are subject to foreign exchange rules. You must have a valid Aadhaar and PAN card. If you’re employed by the government, you’re automatically enrolled in NPS-no action needed.

There’s no upper limit on how much you can contribute annually. But the tax benefits cap out at ₹2 lakh per year (₹1.5 lakh under 80C + ₹50,000 under 80CCD(1B)). Beyond that, your money still grows tax-deferred, but you won’t get a deduction.

Step-by-Step: How to Open an NPS Account Online

Opening an NPS account takes less than 15 minutes if you have your documents ready. Here’s how to do it online:

- Visit the official NPS portal at nps.org.in or go to any registered Point of Presence (PoP) website like ICICI Bank, HDFC Bank, or Axis Bank.

- Click on “Register for NPS” and choose “Individual Subscriber.”

- Enter your details: Full name, date of birth, mobile number, email, and address. Your Aadhaar number will auto-fill your personal details if you’re using the e-KYC option.

- Upload documents: Scan your Aadhaar, PAN, and a recent passport-sized photo. Make sure the photo has a white background and you’re not wearing glasses or a cap.

- Choose your PoP: Pick a bank or financial institution that acts as your service provider. Most people choose their existing bank for convenience.

- Select your investment choice: You can go with Active Choice (you decide the asset allocation) or Auto Choice (the system shifts your portfolio from equity to debt as you age). For beginners, Auto Choice is simpler and safer.

- Set up your first contribution: Minimum initial contribution is ₹500 for Tier I. You can pay via UPI, net banking, or debit/credit card.

- Verify your identity: You’ll receive an OTP on your registered mobile number. Enter it to confirm.

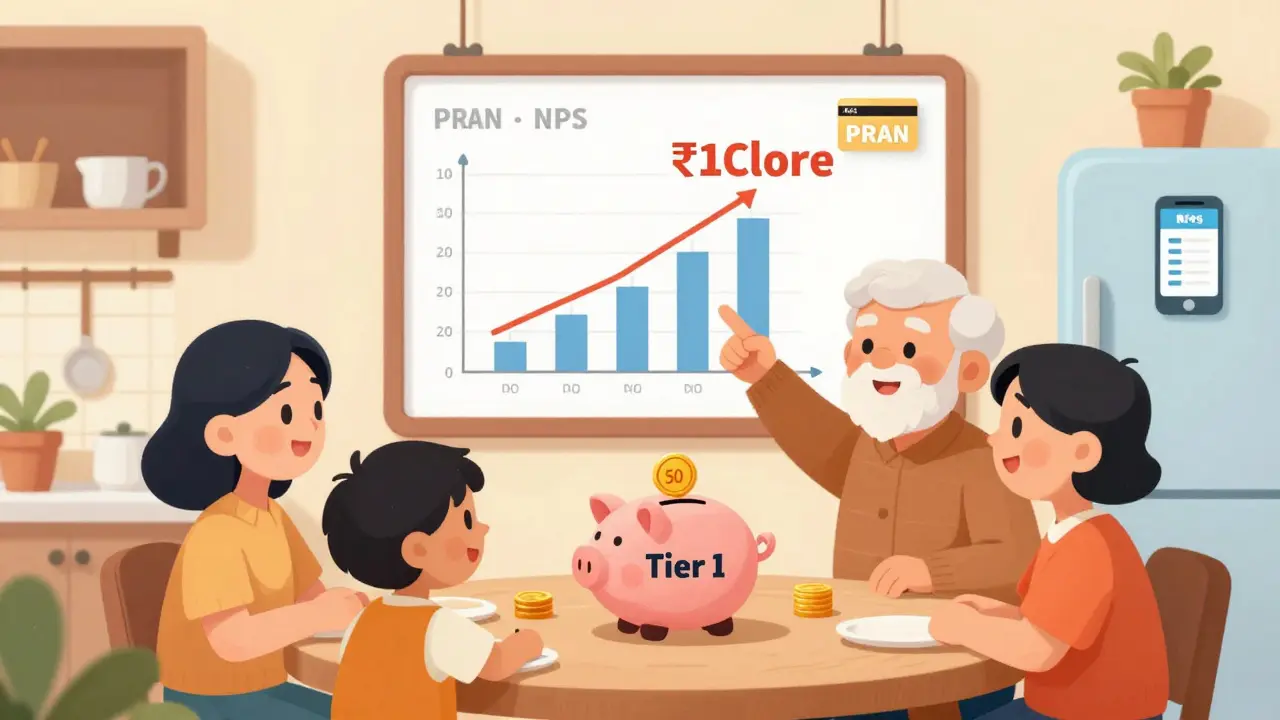

- Receive your PRAN: Within 24 hours, you’ll get a Permanent Retirement Account Number (PRAN) via SMS and email. This is your unique NPS ID. Keep it safe.

Once your account is active, you can log in anytime to check your balance, change your investment mix, or make additional contributions.

How to Contribute to Your NPS Account

Contributing to NPS is easy. You can pay anytime-monthly, quarterly, or annually. The minimum annual contribution for Tier I is ₹6,000 (₹500 per month). If you miss a payment, your account stays active, but you won’t earn interest on the missed amount.

Here’s how to make contributions:

- Log in to your NPS account via the official website or the NPS mobile app.

- Go to “Contribution” and select your account (Tier I or Tier II).

- Enter the amount and choose your payment method: UPI, net banking, or debit card.

- Confirm and pay. You’ll get a receipt with your transaction ID.

You can also set up auto-debit from your bank account so you never forget. Many people link NPS contributions to their salary cycle-just like they do with EMI payments.

Investment Options: How Your Money Grows

NPS gives you three asset classes to invest in:

- E (Equity): Up to 75% of your portfolio can go into stocks and equity mutual funds. Higher risk, higher returns over time.

- C (Corporate Bonds): Medium-risk investments in bonds issued by private companies.

- G (Government Securities): Low-risk, stable returns backed by the Indian government.

If you choose Auto Choice, your allocation changes automatically:

- Up to age 35: 50% E, 30% C, 20% G

- Ages 36-50: 40% E, 30% C, 30% G

- Ages 51-60: 30% E, 30% C, 40% G

- Ages 60+: 10% E, 20% C, 70% G

If you pick Active Choice, you can adjust these percentages anytime. But you can’t go above 75% in equity, and you must hold at least 10% in government securities.

Historical returns over the last 10 years have averaged 8-10% annually, depending on market conditions. That’s higher than fixed deposits and comparable to balanced mutual funds-with much lower fees.

What Happens at Retirement?

At age 60, your NPS account matures. Here’s what you can do:

- Withdraw up to 60% of your total corpus as a lump sum. This amount is completely tax-free if you’ve contributed for at least 10 years.

- Use the remaining 40% to buy an annuity from an IRDA-approved provider. You can choose from lifetime payments, payments for 5-10 years, or payments with a spouse benefit.

- If you want to delay retirement, you can keep contributing until age 70. After that, you must withdraw.

There’s one exception: if your total corpus is less than ₹5 lakh at 60, you can withdraw 100% as a lump sum without buying an annuity. This helps low-income contributors who don’t have enough to sustain a monthly payout.

Common Mistakes to Avoid

Many people open NPS accounts but never contribute regularly. Others pick the wrong investment option and regret it later. Here’s what to watch out for:

- Not contributing enough: ₹500/month won’t get you far. Aim for ₹2,000-₹5,000/month if you want a decent retirement income.

- Ignoring Tier II: If you need emergency cash, Tier II gives you flexibility without breaking your retirement plan.

- Chasing high equity returns too late: If you’re 55 and still investing 70% in stocks, you’re risking your savings right before retirement.

- Forgetting to update your nominee: Always keep your nominee details current. If you don’t, your family might face delays accessing your funds.

How NPS Compares to Other Retirement Options

Let’s say you’re 30 and want to save ₹5,000/month for retirement. Here’s how NPS stacks up:

| Option | Corpus at 60 | Tax Benefits | Liquidity | Withdrawal Rules |

|---|---|---|---|---|

| NPS (Tier I) | ₹78 lakh | Up to ₹2 lakh/year deduction | Low (locked until 60) | 60% lump sum tax-free, 40% annuity |

| PPF | ₹72 lakh | ₹1.5 lakh/year deduction | Medium (partial withdrawals after 7 years) | 100% lump sum tax-free |

| Equity Mutual Funds (ELSS) | ₹78 lakh | ₹1.5 lakh/year deduction | High (no lock-in after 3 years) | Full withdrawal, taxed as capital gains |

| Fixed Deposit | ₹68 lakh | None | High | Full withdrawal, interest taxed annually |

NPS wins on tax efficiency and fees. PPF is safer and more liquid, but offers lower returns. ELSS gives you flexibility but no guaranteed income stream. NPS is the only option that forces you to convert savings into lifelong income.

Next Steps: What to Do After Opening Your NPS Account

Now that your account is active, here’s what to do next:

- Download the NPS mobile app and set up push notifications for contribution reminders.

- Review your investment allocation every year. Adjust it if your risk tolerance changes.

- Link your NPS account to your income tax return so your deductions are auto-filled.

- Share your PRAN with your employer if you’re salaried-some companies offer matching contributions.

- Set a goal: “I want ₹1 crore by 60.” Work backward to figure out how much you need to save monthly.

NPS isn’t magic. It won’t make you rich overnight. But if you start early, contribute consistently, and stay disciplined, it will give you something most people never have: financial security in retirement.

Can I open an NPS account if I’m not an Indian resident?

Yes, Non-Resident Indians (NRIs) can open an NPS account, but they must have a valid Indian bank account and PAN card. Contributions must be made in Indian rupees from an NRE or NRO account. NRIs cannot contribute after turning 60, and withdrawals are subject to foreign exchange regulations. They must also comply with RBI guidelines on repatriation.

Is NPS better than PPF for retirement?

NPS offers higher potential returns due to equity exposure and lower fees, but PPF is safer and more liquid. PPF gives you 100% tax-free lump sum at maturity, while NPS requires you to buy an annuity with 40% of your corpus. If you want guaranteed returns and easy access, PPF is better. If you want higher growth and a structured income stream, NPS wins.

Can I have both Tier I and Tier II NPS accounts?

Yes, you can hold both Tier I and Tier II accounts simultaneously. But you must open Tier I first. Tier II acts as a flexible savings account with no lock-in, but it doesn’t offer tax benefits. Many people use Tier II to park emergency funds or save for short-term goals without touching their retirement corpus.

What happens to my NPS account if I die before 60?

If you pass away before retirement, your entire NPS corpus is paid to your nominee or legal heir. There’s no tax on the amount received by the nominee. You can update your nominee anytime through your NPS account portal. It’s important to keep this information current-especially after marriage, divorce, or the birth of a child.

Can I change my pension fund manager in NPS?

Yes, you can switch your pension fund manager once a year. There are seven approved fund managers like SBI, HDFC, ICICI, and Kotak. You can compare their historical returns on the NPS website and make the switch online. The process takes 7-10 working days. You can also change your investment pattern (Active or Auto) at any time.

Is the annuity payout from NPS taxable?

Yes, the monthly annuity payments you receive after retirement are taxable as income under the head “Income from Other Sources.” The tax rate depends on your income slab in the year you receive the payment. However, the lump sum withdrawal (60%) is tax-free if you’ve contributed for at least 10 years.

Final Thought: Start Now, Even If It’s Small

You don’t need ₹10,000 a month to begin. Even ₹1,000/month invested for 30 years at 8% growth becomes over ₹15 lakh. That’s not enough to retire on, but it’s enough to make a real difference. The biggest mistake people make is waiting until they feel ready. Retirement planning isn’t about timing the market-it’s about timing your start. The earlier you begin, the less you need to save each month. NPS gives you the tools. All you need to do is click “Register” and make that first payment.