Section 54 Exemption in India: How to Avoid Capital Gains on Property Sale

When you sell a property in India and make a profit, the government taxes that gain. It’s called capital gains tax, and it can eat up a big chunk of your profit-sometimes over 20%. But there’s a legal way to avoid paying it entirely: Section 54 of the Income Tax Act. If you know how to use it, you can walk away from a property sale with your full profit intact.

What Is Section 54 Exemption?

Section 54 lets you avoid paying long-term capital gains tax if you use the money from selling your property to buy another one. This isn’t a loophole. It’s a government incentive to encourage reinvestment in residential property. The idea is simple: if you’re moving from one home to another, you shouldn’t be taxed on the profit just because you’re upgrading or relocating.

But there are strict rules. You can’t just sell a property and put the money in a savings account. You have to buy a new residential property in India. And you have to do it within a specific time window. Miss the deadline, and the tax hits you full force.

Who Qualifies for Section 54?

This exemption is only for individuals and Hindu Undivided Families (HUFs). Companies, firms, or trusts can’t use it. You also need to own the property you’re selling for at least 24 months. If you bought it two years ago and sold it now, you’re eligible. If you bought it 18 months ago, you’re not.

The property being sold must be a residential house-apartment, bungalow, or independent house. It doesn’t matter if it was your primary home or a rental. As long as it’s residential, Section 54 applies.

The new property you buy must also be residential. You can’t use the sale proceeds to buy land, a commercial building, or a plot. It has to be a house you can live in-or rent out.

How to Claim the Exemption

There are three ways to claim Section 54, depending on when you buy the new property:

- Buy before selling: You can purchase the new property up to one year before the date you sell the old one. This is rare but legal. People often do this when they’ve already found their next home and just need to close the old sale.

- Buy after selling: You have two years after the sale date to buy the new property. Most people use this window.

- Construct a new house: If you want to build instead of buy, you have three years from the sale date to complete construction. You can’t just buy land-you have to start building and finish within the deadline.

The entire sale amount doesn’t need to be reinvested. You only need to reinvest the amount equal to your capital gain. For example, if you sold a house for ₹80 lakh and your original cost (after indexation) was ₹50 lakh, your gain is ₹30 lakh. You only need to reinvest ₹30 lakh into the new property to get full exemption. Any extra money you put in is a bonus, but not required.

What Happens If You Don’t Reinvest Fully?

If you only reinvest part of the gain, you’ll pay tax on the difference. Say you made ₹30 lakh in gain but only bought a new house for ₹20 lakh. You’ll pay long-term capital gains tax on the remaining ₹10 lakh. The tax rate is 20% with indexation, so you’d owe ₹2 lakh in tax.

There’s a way out, though. If you haven’t bought anything yet but plan to, you can deposit the sale proceeds into a special account called the Capital Gains Account Scheme (CGAS). This is a government-backed savings account that holds your money until you buy the new property. You can’t withdraw it for anything else-not for a car, not for travel, not for business. If you take money out early, the exemption is lost, and you’ll owe tax immediately.

Capital Gains Account Scheme (CGAS): Your Safety Net

CGAS is a lifesaver if you haven’t found your next home yet. You open it at any public sector bank or authorized private bank. There are two types:

- Type A: Savings account. You earn interest like a regular savings account. Good if you’re planning to buy soon.

- Type B: Term deposit. Higher interest, but your money is locked for a fixed period. Best if you’re waiting to build a house.

You must deposit the full amount you plan to reinvest before filing your tax return. If you don’t, the tax department will treat the entire gain as taxable. And once the money is in CGAS, you can’t touch it until you buy or build. Withdrawals are only allowed for property purchases or construction payments.

Many people forget this step. They assume the exemption applies automatically. It doesn’t. If you don’t deposit into CGAS and don’t buy within the time limit, you’ll get hit with tax-and penalties.

What If You Sell and Buy Again Later?

There’s a twist. If you use Section 54 to buy a new house and then sell that house within three years, the exemption is reversed. The government considers this a short-term move. So if you bought a new home in 2024 using Section 54 and sold it in 2026, you’ll have to pay back the tax you avoided.

This rule exists to stop people from using Section 54 as a tax-free cash-out scheme. The government wants you to invest in housing long-term, not flip properties.

That’s why it’s smart to plan ahead. If you think you might need to sell again soon, don’t use Section 54. The tax savings aren’t worth the risk of having to repay later.

Common Mistakes People Make

Even smart investors mess this up. Here are the top three errors:

- Buying a commercial property. You can’t use Section 54 for shops, offices, or warehouses. I’ve seen people buy a ground-floor shop thinking it’s a good investment. It doesn’t count. Only residential.

- Missing the deadline. The two-year window is strict. If you sell in June 2025, you must buy by June 2027. No extensions. No excuses.

- Not using CGAS when needed. If you haven’t found a house yet, deposit the money. Don’t wait. The clock keeps ticking.

Another trap: buying a property in someone else’s name. The law says the new property must be in your name. If you buy it in your child’s name, even if you’re paying, you lose the exemption.

Section 54 vs. Section 54F: Which One to Use?

There’s another rule-Section 54F-that applies if you sell something other than a house, like land or jewelry, and want to buy a house. But if you’re selling a house, Section 54 is your only option. Section 54F has stricter rules: you can’t own more than one house at the time of sale. If you own two homes and sell one, you can’t use 54F. But you can still use 54 if the one you sold was residential.

So if you’re selling a house, forget 54F. Stick to 54. It’s simpler and more flexible.

Real-World Example

Here’s how it works in practice:

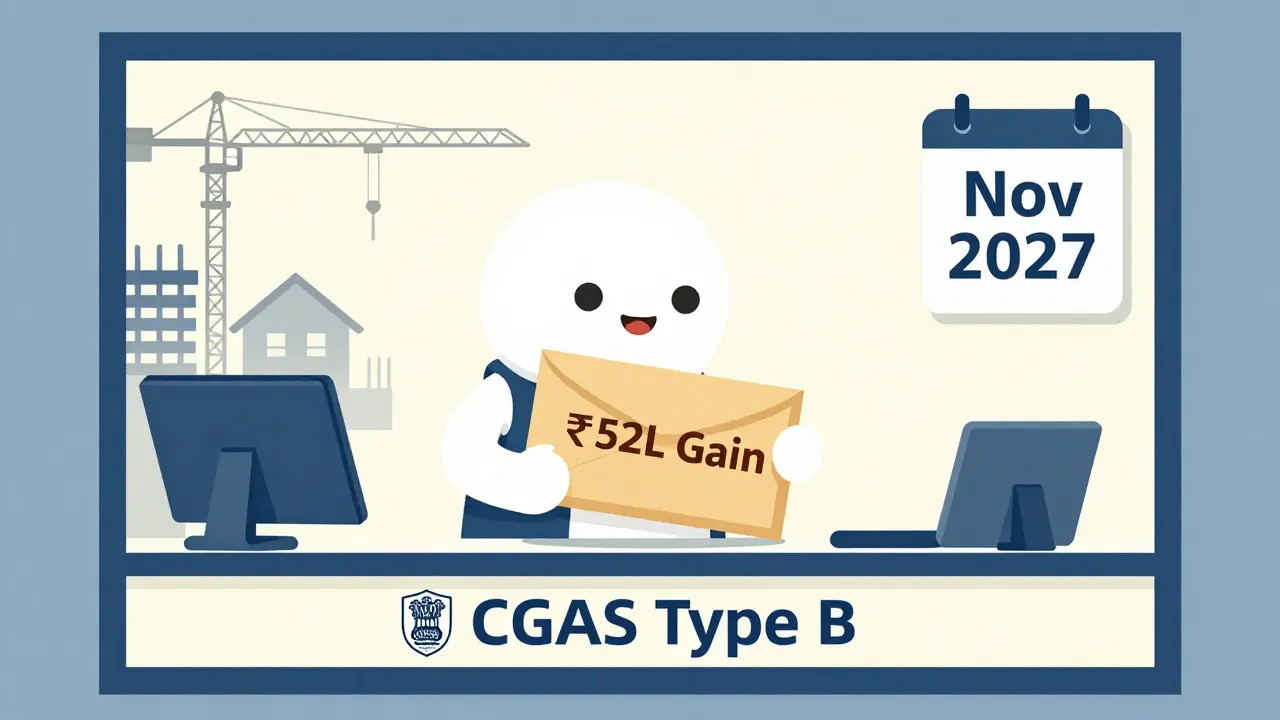

Arjun sold his apartment in Pune in January 2025 for ₹1.2 crore. He bought it in 2015 for ₹45 lakh. After indexation, his cost rose to ₹68 lakh. His capital gain: ₹52 lakh.

He didn’t have a new home lined up. So he deposited ₹52 lakh into a CGAS Type B account in February 2025. He found a plot in Coimbatore in August 2025 and started construction. He completed the house in November 2027-just in time.

He filed his tax return for 2025-26 claiming Section 54 exemption. The tax department accepted it. He paid zero capital gains tax. He saved over ₹10 lakh.

Had he waited until 2028 to finish building? He’d have owed ₹10.4 lakh in tax. The deadline isn’t a suggestion. It’s a hard stop.

What About Inherited Property?

If you inherit a house and sell it, you can still use Section 54. The holding period is calculated from when the original owner bought it. So if your father bought a house in 2008 and you inherited it in 2020, then sold it in 2026, you’ve held it for 18 years. That’s long-term. You can reinvest the gain into a new home and claim exemption.

But you must be the legal owner. If you’re just a nominee or trustee, you can’t claim Section 54.

Final Checklist to Avoid Tax

Before you sell, ask yourself:

- Have I owned this property for more than 24 months?

- Is the property residential?

- Do I have a plan to buy or build another residential property?

- Will I complete the purchase or construction within two years (or three for construction)?

- If I’m not ready to buy yet, have I deposited the gain into CGAS?

- Will the new property be in my name?

If you answered yes to all, you’re good. If even one answer is no, you’re risking a big tax bill.

When Section 54 Doesn’t Help

Section 54 won’t help if:

- You’re selling a commercial property and want to buy a house. Use Section 54F instead.

- You’re selling a house and buying a second home while still owning your first. You can’t claim exemption if you own more than one residential property at the time of purchase.

- You’re selling and using the money for a business, car, or foreign trip. The law requires reinvestment in residential property only.

There’s no workaround. The rules are clear. If you try to bend them, the tax department will catch you.