ELSS vs Tax-Saving FD in India: Which Gives Better Returns, Liquidity, and Safety?

When you're trying to save tax under Section 80C in India, two options keep popping up: ELSS funds and Tax-Saving Fixed Deposits. Both promise deductions up to ₹1.5 lakh a year, but that’s where the similarity ends. One grows your money in the stock market. The other locks it in with guaranteed, but low, interest. Choosing between them isn’t just about tax - it’s about what you want your money to do over the next 10 years.

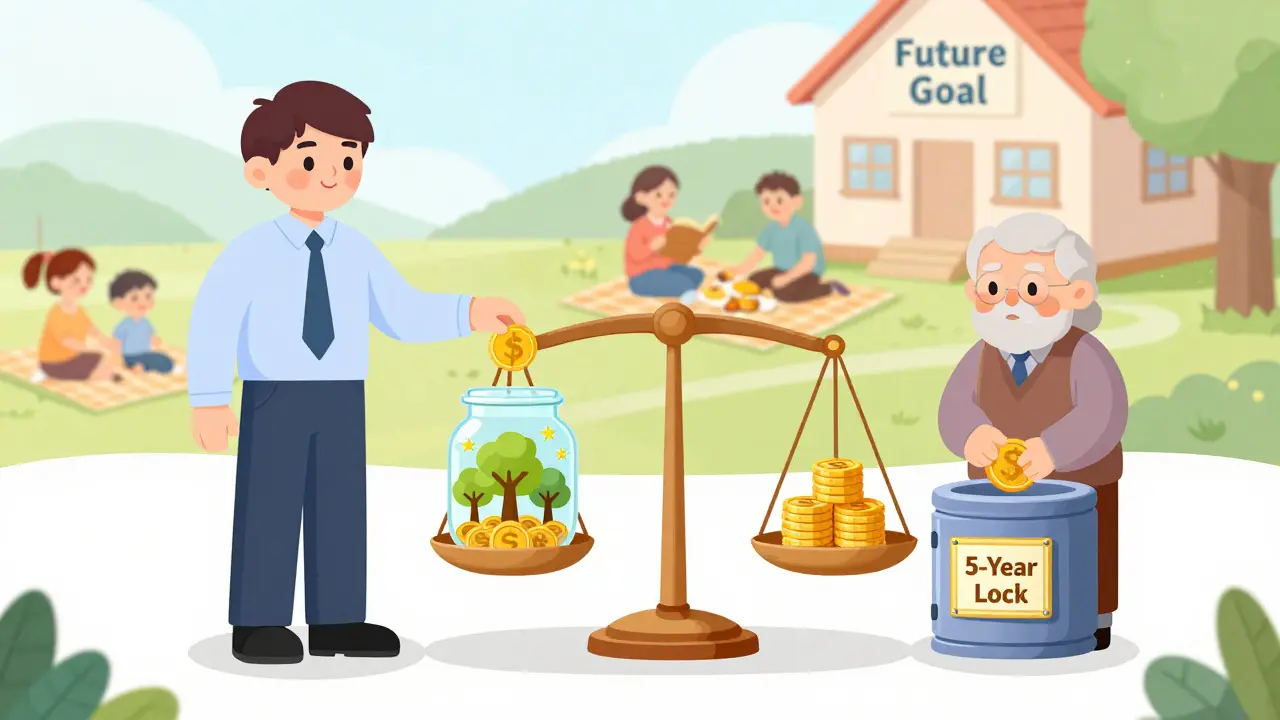

What Exactly Is ELSS?

ELSS stands for Equity Linked Savings Scheme. It’s a type of mutual fund that invests mostly in stocks - at least 80% of its assets. Because it’s equity-based, returns aren’t guaranteed, but historically, ELSS funds have delivered 12% to 15% annual returns over the long term. The tax benefit comes under Section 80C, and you can invest up to ₹1.5 lakh per year to get a full deduction from your taxable income.

Here’s the catch: there’s a mandatory lock-in of three years. You can’t withdraw your money before that. But after three years? You’re free to keep investing or cash out. Many people treat ELSS as a long-term wealth builder, not just a tax tool. A 2023 analysis by AMFI showed that ELSS funds averaged 13.7% CAGR over the last 10 years, beating inflation by a wide margin.

What Is a Tax-Saving FD?

A Tax-Saving Fixed Deposit is exactly what it sounds like: a fixed deposit with a tax break. Banks and post offices offer these, and they’re backed by the government. The interest rate is fixed at the time of deposit - currently between 6.5% and 7.5% for most major banks. Like ELSS, you can invest up to ₹1.5 lakh per year under Section 80C.

The lock-in period here is longer: five years. No early withdrawals. No partial withdrawals. If you break it, you lose the tax benefit and may even have to pay back the deduction with interest. But in return, you get absolute safety. Even if the bank fails, your deposit is insured up to ₹5 lakh under DICGC. That’s the kind of peace of mind you can’t get from stocks.

Return Comparison: Growth vs. Guaranteed

Let’s say you invest ₹1.5 lakh every year for five years. Here’s what you’d end up with:

| Investment Type | Annual Return | Total Invested | Projected Value After 5 Years |

|---|---|---|---|

| ELSS (13% avg) | 13% | ₹7.5 lakh | ₹9.8 lakh |

| Tax-Saving FD (7% avg) | 7% | ₹7.5 lakh | ₹8.4 lakh |

That’s ₹1.4 lakh more in your pocket with ELSS - just from returns. And that’s without compounding beyond five years. If you hold ELSS for 10 years, the gap widens to over ₹4 lakh. Tax-Saving FDs won’t ever beat inflation consistently. ELSS has done it for decades.

Liquidity: Lock-In Matters More Than You Think

Both have lock-ins, but they’re not the same. ELSS locks your money for three years. Tax-Saving FD for five. That’s two extra years your cash is stuck.

Imagine you need money in year four because of a medical emergency or a sudden business opportunity. With ELSS, you’re free to withdraw. With Tax-Saving FD? You’re stuck. You can’t even take a loan against it - unlike regular FDs, which often allow borrowing up to 90% of the deposit value.

ELSS also lets you invest via SIPs. You can start with ₹500 a month. That’s flexible, manageable, and spreads risk. Tax-Saving FDs require a lump sum upfront. If you don’t have ₹1.5 lakh ready in April, you’re out of luck for that year’s deduction.

Risk: Can You Handle Market Swings?

ELSS is not for everyone. If the market drops 20% in a year, your portfolio drops too. In 2022, many ELSS funds lost 15-20% in the first half - then recovered and ended the year up 10%. If you panic-sell during a dip, you lose. If you hold through the cycle, you win.

Tax-Saving FDs don’t have that problem. Your principal is safe. Interest is fixed. No surprises. But here’s the hidden risk: inflation. At 6% interest and 7% inflation, your real return is negative. Your money loses purchasing power every year. Over five years, that’s a 30% erosion in what your savings can buy.

ELSS fights inflation. Tax-Saving FDs surrender to it.

Who Should Choose What?

Choose ELSS if:

- You’re investing for 7+ years

- You understand markets can go down - but you won’t panic

- You want growth, not just tax savings

- You can invest regularly via SIP

Choose Tax-Saving FD if:

- You hate any risk to your principal

- You need guaranteed returns for a short-term goal (like a child’s school fee in 5 years)

- You’re risk-averse and don’t want to check your portfolio monthly

- You’re nearing retirement and can’t afford losses

Most people in their 30s and 40s should lean toward ELSS. The longer your time horizon, the more power compounding has. Even if you start with ₹5,000 a month in ELSS, in 15 years, you could have over ₹30 lakh - and pay zero tax on the gains after the lock-in.

What About Tax on Gains?

This is a big one. ELSS gains are taxed. If you sell after one year, it’s long-term capital gains. The first ₹1 lakh is tax-free. Anything above that? 10% tax. No indexation. That’s it. No TDS. No complex filing.

Tax-Saving FDs? Interest is fully taxable every year. Even if you don’t withdraw it, the bank issues a TDS certificate, and you pay tax on it as per your slab. So if you’re in the 30% tax bracket, you’re giving back almost a third of your interest income every year. That’s a hidden cost.

ELSS wins here too - you defer tax until you sell, and you get a free ₹1 lakh exemption.

Final Decision: It’s Not About Tax - It’s About Time

Section 80C is a tool. But the real question is: what do you want your money to do?

If you’re looking for safety and simplicity, Tax-Saving FD works. But you’re trading growth for peace of mind. You’ll end up with less money, and your savings will buy less over time.

If you’re willing to ride out market ups and downs, ELSS is the smarter move. It’s not just a tax-saving instrument - it’s a wealth-building engine. The three-year lock-in is a gift. It forces you to stay invested. And in the stock market, time is your biggest advantage.

Don’t pick one just because it’s ‘safe.’ Pick the one that aligns with your life goals. Most people use ELSS for retirement, children’s education, or buying a home. They use Tax-Saving FDs for goals that are five years away and non-negotiable - like a down payment on a flat.

There’s no wrong choice. But there’s a smarter one - and it depends on how long you’re willing to wait.

Can I invest in both ELSS and Tax-Saving FD in the same year?

Yes, you can. The total deduction under Section 80C is capped at ₹1.5 lakh per year. So if you invest ₹1 lakh in ELSS and ₹50,000 in Tax-Saving FD, you still get the full ₹1.5 lakh deduction. But your total investment across all 80C instruments - including PPF, NSC, life insurance, etc. - cannot exceed ₹1.5 lakh.

Is ELSS riskier than mutual funds?

ELSS is a type of equity mutual fund, so it carries the same risk as any other diversified equity fund. The only difference is the three-year lock-in. That lock-in actually reduces risk over time because it prevents emotional selling during market dips. Many investors who stay invested in ELSS for 7+ years see positive returns in 9 out of 10 years.

Can I withdraw from ELSS before 3 years?

No. The lock-in period is legally mandated. If you try to withdraw early, the fund house will reject the request. Even if you redeem by mistake, the amount will be reversed, and you’ll lose the tax benefit. The only exception is in case of death - then the nominee can withdraw.

Which gives better returns: ELSS or PPF?

Over 10 years, ELSS has consistently outperformed PPF. PPF offers around 7.1% interest (as of 2025), while ELSS averages 12-14%. PPF has a 15-year lock-in, which is much longer. If you’re looking for growth, ELSS wins. If you want guaranteed returns and a longer-term savings plan, PPF is safer but slower.

Is ELSS better than NSC for tax saving?

Yes, for most people. NSC offers around 7.7% interest, locked in for 5 years. Like Tax-Saving FD, the interest is taxable every year. ELSS has higher returns, shorter lock-in, and tax-free gains after ₹1 lakh. NSC is only better if you absolutely refuse to touch equity markets - but even then, the returns are lower and the tax treatment is worse.

Next Steps: What to Do Today

Check your current 80C investments. If you’re only using Tax-Saving FDs and you’re under 45, you’re leaving money on the table. Start a monthly SIP in a top-performing ELSS fund - even ₹2,000. Pick one with a 10-year track record of consistent returns. Look at funds like Parag Parikh Flexi Cap, Axis Long Term Equity, or ICICI Prudential Long Term Equity.

If you’re over 55 and retired, stick with Tax-Saving FDs. But don’t forget to reinvest the interest elsewhere - maybe in a short-term debt fund - to beat inflation.

And if you’re unsure? Split it. Put 70% in ELSS and 30% in Tax-Saving FD. That way, you get growth with a safety net. The goal isn’t to pick the perfect option. It’s to pick the one that matches your life - not your fear.