Joint Property Ownership in India: A Guide to Legal, Tax, and Financial Rules

Joint Property Ownership in India is more than just a shared mortgage; it is a legal arrangement that defines the rights and liabilities of multiple individuals over a single piece of real estate. Whether you're looking to split the financial burden or build a family legacy, understanding the nuances of Indian property law is non-negotiable.

The Different Ways to Own Property Jointly

Before you sign anything, you need to know that not all "joint ownership" is created equal. Depending on how the title is registered, your rights to the property change drastically.

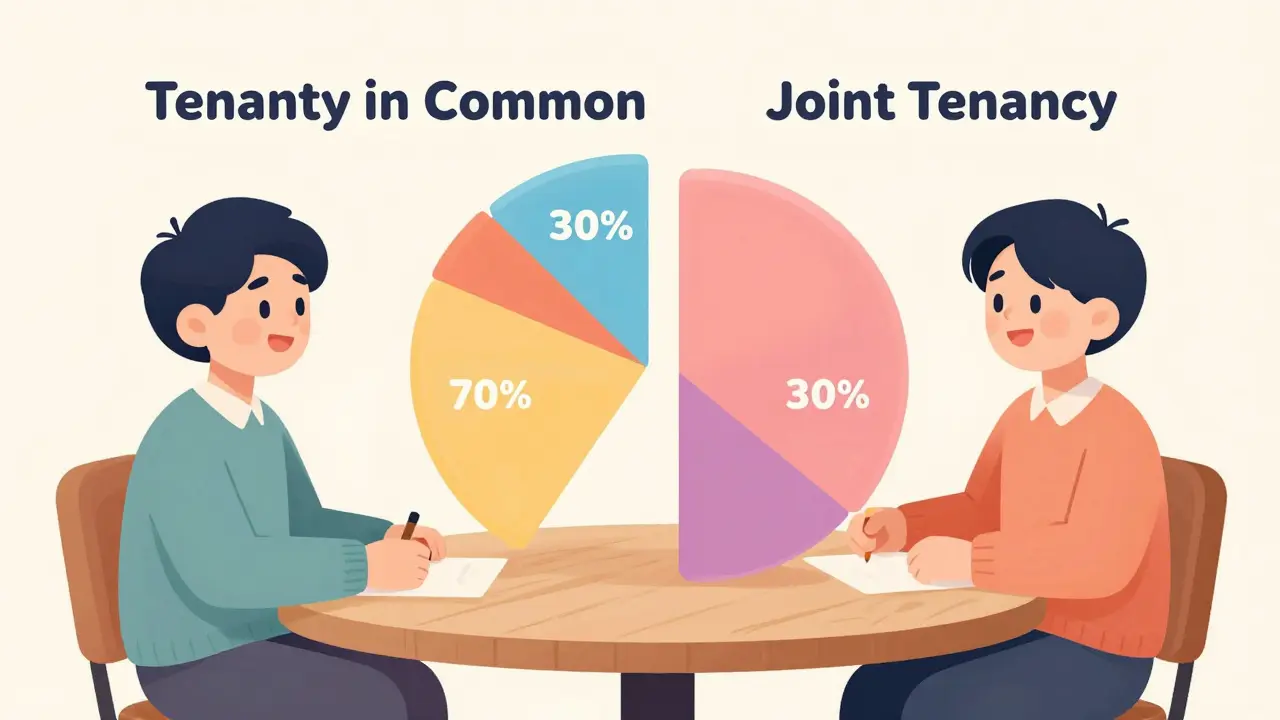

Tenancy in Common is the most frequent form of co-ownership where each person owns a specific share of the property. These shares don't have to be equal. For example, if you provide 70% of the funds and your partner provides 30%, your ownership stakes reflect that. Crucially, if one owner passes away, their share goes to their legal heirs, not automatically to the other co-owners.

Joint Tenancy is a stricter arrangement where owners hold an equal interest in the entire property. The defining feature here is the "right of survivorship." If one joint tenant dies, their interest automatically transfers to the surviving owner, regardless of what their will says. This is common among spouses who want the home to pass seamlessly to the survivor.

Then there is the concept of Coparcenary rights, which are unique to Hindu Law. In a Hindu Undivided Family (HUF), property is often owned collectively by members of the family. Since the 2005 amendment to the Hindu Succession Act, daughters have equal rights as sons in ancestral property, changing the dynamic of how family estates are managed today.

| Feature | Tenancy in Common | Joint Tenancy | Coparcenary (HUF) |

|---|---|---|---|

| Ownership Share | Can be unequal | Must be equal | By birthright/lineage |

| Right of Survivorship | No (goes to heirs) | Yes (goes to co-owner) | Varies by law/partition |

| Transferability | Easier to sell share | Requires consent | Complex (requires partition) |

Tax Implications and the Income Tax Act

The Indian government actually provides some decent incentives for joint ownership, provided you're a "co-owner" and not just a "joint holder." There is a massive difference between the two. A joint holder is often just added for convenience, while a co-owner has contributed to the purchase price.

Under the Income Tax Act, 1961, co-owners can each claim tax deductions on their share of the home loan. If you and your spouse are both earning members and co-owners, you can both claim deductions under Section 80C for the principal repayment and Section 24(b) for the interest payment. This effectively doubles the tax-saving potential of a single property.

But watch out for the "clubbing of income" rules. If you transfer a property to your spouse without adequate consideration (essentially for free), any rental income generated from that property might be "clubbed" with your income. The Income Tax Department does this to prevent people from shifting assets to family members in lower tax brackets to avoid paying more tax.

When it comes to selling, Capital Gains Tax is calculated based on your individual share. If you own 50% of a flat and sell it, you are responsible for the tax on the gain derived from your 50% portion. You can offset this by investing the gain into another residential property under Section 54 or by buying specific bonds under Section 54EC.

Financial Logistics: Mortgages and Liabilities

Banks love joint applications. Why? Because it lowers their risk. If you apply for a home loan with a co-applicant, the bank can combine both incomes to determine eligibility, which usually allows you to qualify for a higher loan amount.

However, this is a double-edged sword. In the eyes of the lender, you are "jointly and severally liable." This means if your co-owner stops paying their share of the EMI, the bank doesn't care who is at fault-they will come after you for the full payment. Your credit score is tied to the payment history of the property, regardless of whether you're the primary borrower or just a co-signatory.

A common mistake is ignoring the "exit strategy." What happens if you have a falling out with your business partner? Or if a sibling decides they want their money back? Without a written agreement, the only way to split a physical house is to sell it and divide the cash, or go through a grueling legal partition suit in court.

The Legal Paperwork You Can't Skip

The title deed is your primary shield. Ensure that the Sale Deed clearly specifies the percentage of ownership for each person. If the deed says "jointly owned" without specifying percentages, the law typically presumes equal ownership, which might not be fair if one person paid 90% of the cost.

For those investing with friends or partners, a

Co-ownership Agreement is vital. This is a private contract that governs the "what-ifs." It should cover:

Registration is the final hurdle. In India, any property transfer must be registered at the local sub-registrar's office and the appropriate Stamp Duty must be paid. Be aware that stamp duty rates can vary; in some states, registering a property in a woman's name attracts a lower stamp duty rate, which is a smart financial move for families.

Common Pitfalls and How to Avoid Them

Many people confuse "joint names on a bank account" with "joint ownership of a house." Just because your name is on the utility bill doesn't mean you have a legal claim to the property. Only the registered deed counts.

Another trap is the "benami" property issue. The Benami Transactions (Prohibition) Act prohibits buying property in someone else's name to hide the real owner's identity or to park unaccounted money. If you provide all the funds but put the house in a distant relative's name to save tax, you risk losing the property entirely and facing heavy penalties.

Lastly, don't forget about the Society Transfer Fee. If the property is part of a Co-operative Housing Society, adding a name to the deed is only half the battle. You must also get the society's membership updated, or you'll face issues when trying to sell the property later.

Can I remove a co-owner's name from the property deed?

Yes, but it requires the co-owner's consent. This is usually done through a "Release Deed" or a "Gift Deed," where one person transfers their interest to the other. This process must be registered and may involve paying stamp duty depending on the relationship between the parties.

How is rental income taxed in joint ownership?

Rental income is split according to the ownership share. If you own 50% of the property, you report 50% of the rent as income. You can then deduct 30% as a standard deduction for repairs and maintenance, as per the Income Tax Act.

What happens to a joint property if one owner dies without a will?

It depends on the ownership type. In a Joint Tenancy with survivorship, the property goes to the surviving owner. In a Tenancy in Common, the deceased owner's share is distributed among their legal heirs according to personal succession laws (e.g., the Hindu Succession Act).

Can a non-resident Indian (NRI) co-own property with an Indian resident?

Yes, NRIs can co-own residential and commercial property in India. However, they must comply with FEMA (Foreign Exchange Management Act) regulations regarding the remittance of funds and the repatriation of sale proceeds.

Who is responsible for the home loan if one co-applicant defaults?

Both co-applicants are jointly and severally liable. This means the bank can demand the entire outstanding amount from either individual, regardless of who was "supposed" to pay the monthly installment.

Next Steps and Troubleshooting

If you're currently in the process of buying a joint property, start by drafting a simple memorandum of understanding (MOU). List exactly who is paying what and how the property will be handled in the event of a dispute. It feels awkward to talk about failure when you're excited about a new home, but it's the only way to protect your investment.

If you've already bought a property and realize the ownership structure is wrong-for example, you paid for it but your name isn't on the deed-don't panic. You can rectify this through a "Rectification Deed" or by executing a fresh gift deed, though this may trigger stamp duty costs. Always consult a local property lawyer to ensure the changes are legally binding and don't trigger unexpected tax liabilities.