SEBI Mutual Fund Categories in India: Understanding Large-Cap, Mid-Cap, and Thematic Funds

When you invest in mutual funds in India, you’re not just picking a fund name-you’re choosing a bet on how the market works. SEBI, the Securities and Exchange Board of India, doesn’t just oversee these funds; it defines them. And those definitions matter. If you don’t know the difference between a large-cap fund and a thematic fund, you could end up with a portfolio that doesn’t match your goals-or your risk tolerance.

What SEBI Says About Mutual Fund Categories

In 2021, SEBI forced a major cleanup of mutual fund schemes. Before that, there were over 2,000 schemes-many with confusing names and overlapping strategies. Investors were lost. So SEBI stepped in and grouped all equity mutual funds into just 11 clear categories. This wasn’t just bureaucracy. It was about giving you real clarity.

Now, every fund has to stick to its category. A large-cap fund can’t suddenly start buying small stocks. A thematic fund can’t pretend to be diversified. That means you can compare funds more easily. You know what you’re getting.

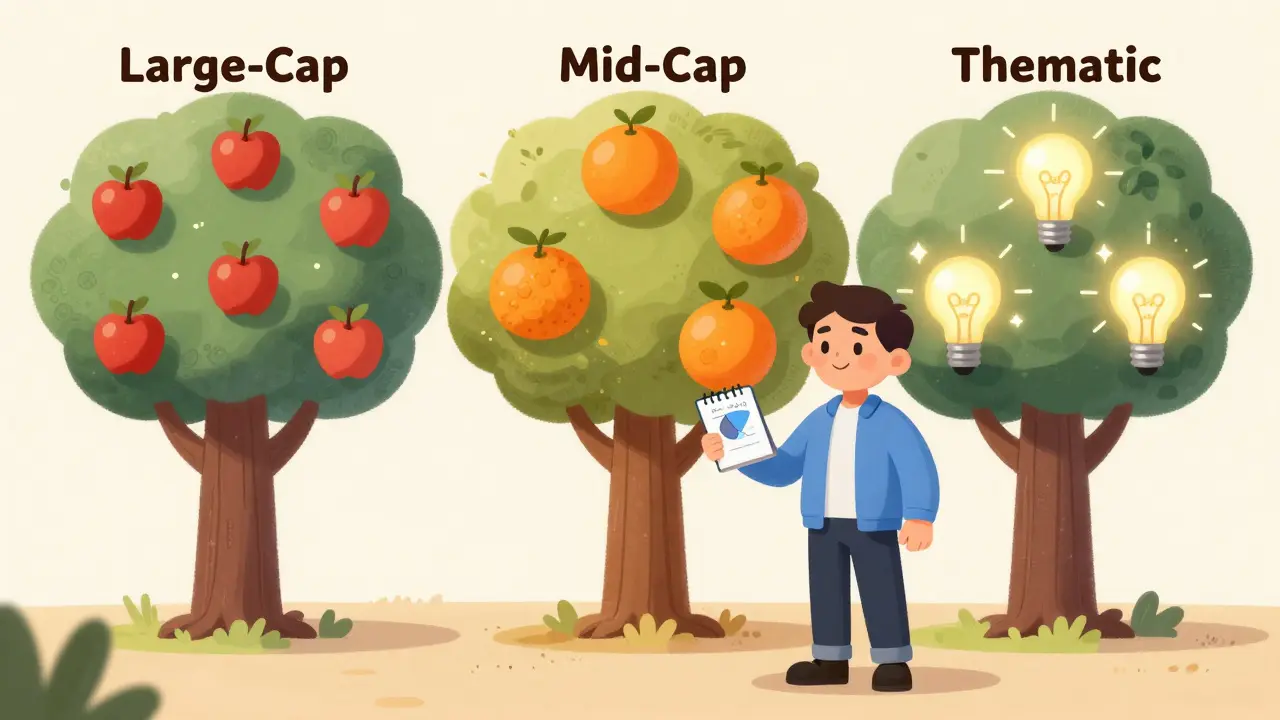

Large-Cap Funds: The Steady Giants

Large-cap funds invest in the biggest companies in India-those ranked in the top 100 by market value. These are names you hear every day: Reliance, HDFC Bank, Infosys, TATA Motors. These companies are stable. They’ve survived economic swings, political changes, and global shocks.

Why do people choose them? Because they’re predictable. Large-cap funds don’t shoot for the moon. They aim for steady growth. Over the last 10 years, the average large-cap fund returned about 12% annually. Not the highest, but with less volatility than other types.

If you’re new to investing, or you’re saving for something like retirement in 15+ years, large-cap funds are your anchor. They won’t make you rich overnight, but they won’t wipe out your savings either.

Mid-Cap Funds: The Growth Engines

Mid-cap funds focus on companies ranked between 101 and 250 in market value. These are the companies that have outgrown startups but haven’t yet become industry giants. Think of companies like Polaris, Astral, or Eicher Motors-solid businesses with room to grow.

Here’s the trade-off: mid-cap funds can deliver higher returns than large-cap funds. Over the past decade, the average mid-cap fund returned nearly 16% annually. But that comes with more risk. These companies are more sensitive to interest rates, supply chain issues, or changes in consumer demand.

If you’re in your 30s or 40s and can handle some ups and downs, mid-cap funds can be a powerful part of your portfolio. They’re not for panic-sellers. If the market drops 10% and you pull out, you’ll miss the rebound. These funds need time-usually 5 to 7 years-to show their full potential.

Thematic Funds: Betting on Trends

Thematic funds don’t care about company size. They care about ideas. They invest in companies tied to a single theme-like electric vehicles, renewable energy, digital payments, or healthcare innovation.

For example, a fund focused on electric vehicles might hold shares in Tata Motors, Exide Industries, Amara Raja Batteries, and even software firms building EV charging apps. It’s not about market cap. It’s about the trend.

Thematic funds can explode in value. The clean energy theme fund launched in 2022 returned over 40% in its first year. But they can also crash. If the theme falls out of favor-like crypto or metaverse funds did in 2022-your money can drop fast.

These aren’t core holdings. They’re satellite bets. Put no more than 10% of your portfolio into thematic funds. And never invest because a YouTube video told you to. Do your own research. Check the fund’s holdings. See if the theme has real demand, not just hype.

How to Choose Between Them

Here’s a simple way to think about it:

- Large-cap: Stability. Low risk. Slow and steady growth. Best for long-term investors who want to sleep well at night.

- Mid-cap: Growth. Medium risk. Higher returns over time. Best for investors with a 5+ year horizon who can ride out market dips.

- Thematic: High risk, high reward. Not for everyone. Best for investors who understand the trend and are ready to lose part of their investment.

Most people should start with a mix of large-cap and mid-cap. Maybe 60% large-cap, 30% mid-cap. Then, if you’re comfortable, add 10% thematic. That’s a balanced approach.

Don’t chase returns. Don’t switch funds every time one underperforms. Look at the fund’s track record over 5 years-not just the last 6 months. Check the expense ratio. A fund charging 2.5% fees will eat into your gains faster than you think.

What to Watch Out For

Some fund houses still try to trick you. They’ll rename a mid-cap fund as a “growth opportunity fund” and charge higher fees. SEBI’s rules help, but you still need to read the factsheet. Look at the portfolio. What stocks are in it? What percentage is in large, mid, and small caps?

Also, avoid funds that say they’re “multi-cap” but mostly hold large-cap stocks. That’s misleading. SEBI requires multi-cap funds to hold at least 25% each in large, mid, and small caps. If a fund doesn’t meet that, it’s breaking the rules.

And don’t ignore taxes. Equity mutual funds held for more than a year are taxed at 10% on gains over ₹1 lakh. Short-term gains (under a year) are taxed at 15%. Factor that into your returns.

Real Examples from 2025

Take the Nippon India Large Cap Fund. It’s been around for 15 years. Its top holdings include Reliance, HDFC Bank, and ICICI Bank. It returned 11.3% annually over the last five years. Low volatility. Consistent.

Compare that to the Axis Mid Cap Fund. It held companies like Bajaj Finance and Divi’s Laboratories. Over five years, it returned 15.7%. But in 2023, it dropped 18% in one quarter. Investors who held on saw it bounce back.

Now look at the Motilal Oswal Electric Vehicles & Future Mobility Fund. It launched in 2022. By early 2025, it had returned 38% total. But in 2024, it fell 22% after battery supply issues hit global EV makers. That’s thematic investing.

Where to Start

If you’re new, start with a large-cap index fund. It’s cheap, transparent, and tracks the market. You don’t need to pick the best fund-just a good one. Then, after a year or two, add a mid-cap fund. Only after you’ve built a habit of investing should you consider thematic funds.

Use platforms like CAMS or KFIN Technologies to check fund holdings. Read the fact sheet. Don’t rely on apps that just show star ratings. Ratings don’t tell you if a fund is still aligned with its category.

And remember: your goal isn’t to beat the market. It’s to build wealth over time. SEBI’s categories exist to help you do that-without getting lost in noise.

What’s the difference between large-cap and mid-cap funds?

Large-cap funds invest in India’s top 100 companies by market value-like Reliance and HDFC Bank. They’re stable and less volatile. Mid-cap funds invest in companies ranked 101 to 250. These are growing businesses with higher return potential but more risk. Large-cap is for steady growth; mid-cap is for higher returns over 5+ years.

Are thematic funds safe for beginners?

No. Thematic funds are high-risk and should only make up a small part of your portfolio-no more than 10%. They’re tied to trends like EVs or AI, which can boom or crash quickly. Beginners should start with large-cap and mid-cap funds to learn how markets work before betting on trends.

Can a fund change its category after I invest?

No. Since SEBI’s 2021 rules, funds must stick to their declared category. If a fund was labeled as a large-cap fund, it can’t suddenly shift to mid-cap without notifying you and giving you a chance to exit without penalty. Always check the fund’s factsheet annually to confirm its holdings still match its category.

How do I know if a fund is truly following SEBI’s rules?

Look at the fund’s portfolio on the AMC’s website or platforms like CAMS. For example, a large-cap fund must hold at least 80% in top 100 stocks. A mid-cap fund must hold at least 65% in stocks ranked 101-250. If the fund’s holdings don’t match, it’s not compliant. You can also check SEBI’s website for category guidelines.

Should I invest in multiple funds from the same category?

Not usually. Two large-cap funds will likely hold the same top stocks-like Reliance, HDFC Bank, and Infosys. Holding both doesn’t give you more diversification; it just doubles your fees. Pick one strong fund per category and stick with it. Focus on low expense ratios and consistent performance over 5+ years.

If you’re building wealth in India, understanding SEBI’s mutual fund categories isn’t optional-it’s essential. You don’t need to be a finance expert. You just need to know what you’re buying. Pick the right category. Stick with it. Let time do the work.