Section 80C for NRIs in India: What Deductions Are Allowed and What’s Not

If you're an NRI living abroad but still have income or investments in India, understanding Section 80C of the Income Tax Act isn't just helpful-it can save you thousands every year. But here's the catch: not everything that works for residents in India works for you. Many NRIs assume they can claim the same deductions as Indian residents, only to get hit with a surprise tax bill. Let’s cut through the noise and lay out exactly what you can and can't claim under Section 80C as an NRI.

What Is Section 80C Anyway?

Section 80C lets you reduce your taxable income in India by up to ₹1.5 lakh per year if you invest in certain approved instruments. It's not a tax exemption-it's a deduction. That means you subtract what you put into these options from your total income before the tax man calculates what you owe. For example, if you earn ₹12 lakh in India and invest ₹1.5 lakh in eligible Section 80C options, your taxable income drops to ₹10.5 lakh. Simple. But for NRIs, the rules have hidden traps.

Eligible Investments Under Section 80C for NRIs

Here’s the good news: most of the major Section 80C options are open to NRIs. You can claim deductions for:

- Public Provident Fund (PPF) - If you opened a PPF account before becoming an NRI, you can keep contributing until it matures. But you cannot open a new PPF account as an NRI. Some banks let you continue deposits if the account was active before your status changed.

- Employee Provident Fund (EPF) - If you're employed in India and contributing to EPF, those contributions count. Even if you're working abroad for an Indian company, your EPF contributions are eligible as long as they're deducted from your Indian salary.

- Life Insurance Premiums - Premiums paid for life insurance policies on your own, your spouse, or your children qualify. The policy must be issued by an Indian insurer. Policies bought overseas don't count.

- Fixed Deposits (FDs) - Five-year tax-saving FDs offered by Indian banks (not post offices) are eligible. Make sure it's labeled as "Tax Saving FD"-regular FDs won't qualify.

- Equity Linked Savings Scheme (ELSS) - These are mutual funds with a three-year lock-in. They're among the most popular because they offer growth potential. NRIs can invest in ELSS through NRE or NRO accounts.

- Tuition Fees - Payments made for full-time education of up to two children in India qualify. The school must be registered in India. Private coaching centers? Not eligible.

- Principal Repayment on Home Loan - If you own a home in India and are paying EMIs, the principal portion of your payment counts toward Section 80C. Interest paid doesn't count here-it's covered under Section 24.

What NRIs Cannot Claim Under Section 80C

Now the bad news: some things you might think are eligible, aren't. Here’s what doesn’t work:

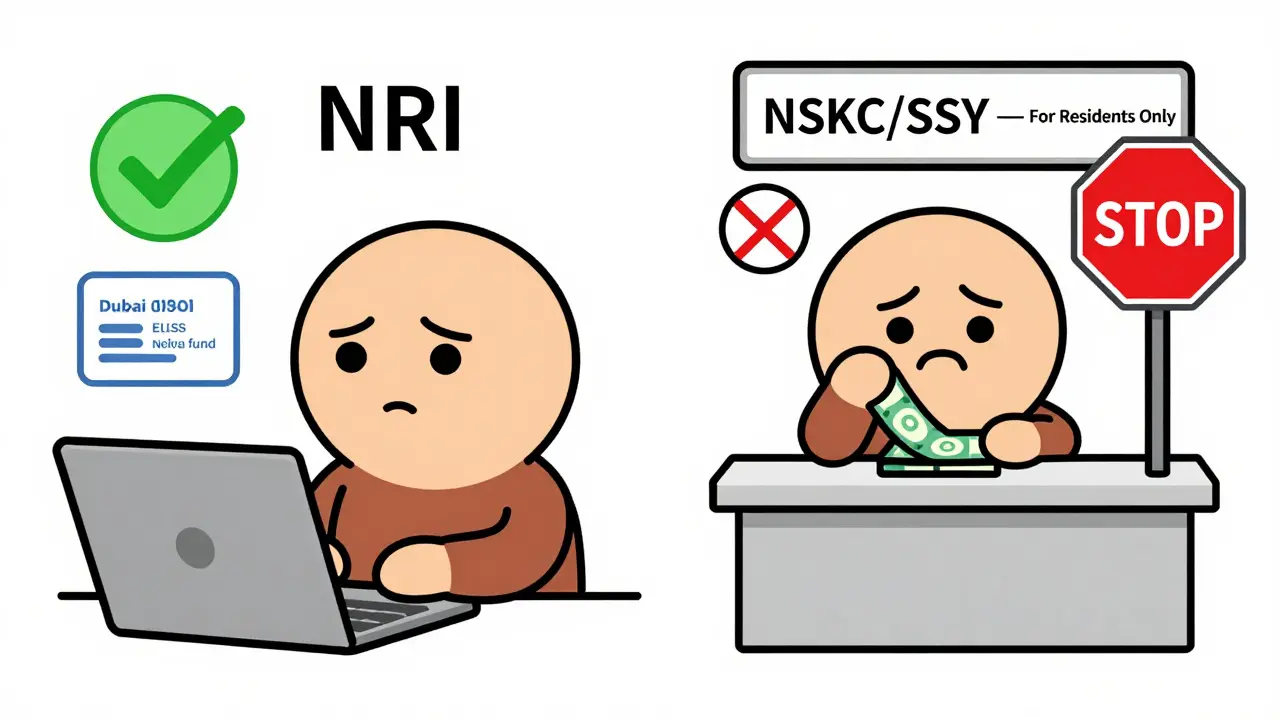

- New PPF accounts - Once you become an NRI, you can't open a new PPF. Even if you try to transfer funds from abroad, banks will reject it. The rule is strict: only Indian residents can open new accounts.

- Post Office Savings Schemes - NSC, Senior Citizen Savings Scheme, or Monthly Income Plans-none are available to NRIs. These are strictly for residents.

- Five-year Sukanya Samriddhi Yojana (SSY) - This is only for parents of girl children who are Indian residents. NRIs can't open or contribute to SSY accounts.

- Contributions to Non-Indian Insurance Policies - If you bought a life insurance policy from a foreign company (say, in the US or Australia), it doesn't count. The policy must be issued by an Indian insurer registered with IRDAI.

- Donations to Charities - While donations under Section 80G are allowed for NRIs, they're separate from Section 80C. Don't confuse the two.

How to Claim Section 80C as an NRI

Claiming this deduction isn't complicated, but you need the right documents. Here's how:

- Keep receipts for all investments-insurance premiums, FD certificates, mutual fund statements.

- Ensure your investments are made from an NRE or NRO account. Don't use a regular savings account in India unless you're still a resident for tax purposes.

- File your income tax return in India using ITR-2 or ITR-3 (depending on whether you have business income).

- Under the "Deductions under Chapter VI-A" section, list your Section 80C investments. The system will auto-calculate the ₹1.5 lakh limit.

- If you're taxed in both India and your country of residence (like Australia or the US), use the Double Taxation Avoidance Agreement (DTAA) to avoid paying twice. India has DTAA with over 85 countries.

Common Mistakes NRIs Make

Here are the top three errors I see NRIs make:

- Assuming PPF is still openable - Many NRIs try to open a new PPF account after moving abroad. Banks will reject it. If you had one before, keep contributing-but don't expect to open a new one.

- Investing in non-eligible instruments - Some NRIs buy foreign mutual funds thinking they’re "similar" to ELSS. They’re not. Only Indian mutual funds registered with SEBI qualify.

- Missing the deadline - Section 80C deductions apply to the financial year ending March 31. If you wait until April to invest, you lose the benefit for the previous year. Plan ahead.

Can You Claim Section 80C If You’re Not Earning in India?

Short answer: no. Section 80C only reduces your taxable income in India. If you have zero income from Indian sources-no rental income, no interest, no salary-you don’t have anything to deduct from. You can’t create a tax loss just to claim 80C. You need taxable income first.

For example, if you own a flat in Mumbai that earns ₹80,000 in rent after expenses, you can use ₹80,000 of your ₹1.5 lakh limit to reduce that taxable rent. But if you have no Indian income at all, Section 80C doesn’t apply.

What About NRE vs NRO Accounts?

This matters. You can invest in Section 80C instruments using either an NRE or NRO account. But there’s a difference:

- NRE account - Funds are repatriable. Interest is tax-free. Ideal for investing in ELSS, tax-saving FDs, or EPF contributions from foreign income.

- NRO account - Funds are non-repatriable without RBI approval. Interest is taxable in India. Still eligible for 80C, but you’ll need to file returns if interest exceeds ₹2.5 lakh.

Most NRIs use NRE accounts for 80C investments because they’re cleaner and tax-efficient. Just make sure the investment is made from the account in your name.

Real-Life Example

Meet Priya, an NRI in Toronto. She earns ₹14 lakh in India from rental income and has ₹1.2 lakh in ELSS investments and ₹20,000 in life insurance premiums. She also repaid ₹1.3 lakh in home loan principal. Total Section 80C claims: ₹1.2L + ₹20K + ₹1.3L = ₹2.7L. But the cap is ₹1.5L. So she can only claim ₹1.5L. She picks the highest-value options: ₹1.2L in ELSS and ₹30K in principal repayment. Her taxable income drops from ₹14L to ₹12.5L. At 20% tax, that’s ₹30,000 saved.

What If You Return to India?

If you become a resident again, your existing Section 80C investments remain valid. You can resume claiming deductions as before. PPF accounts you held as an NRI can continue until maturity. EPF contributions can restart. Just update your residential status with your bank and tax advisor.

Can NRIs open a new PPF account?

No, NRIs cannot open a new PPF account. Only Indian residents are eligible. If you opened a PPF account before becoming an NRI, you can continue contributing until maturity, but you cannot open a new one.

Can NRIs invest in ELSS mutual funds?

Yes, NRIs can invest in ELSS mutual funds through NRE or NRO accounts. These qualify under Section 80C with a three-year lock-in period. Make sure the fund is registered with SEBI and offered by an Indian asset management company.

Are life insurance policies bought overseas eligible for Section 80C?

No. Only life insurance policies issued by Indian insurers registered with IRDAI qualify for Section 80C deductions. Policies from foreign companies-even if they cover Indian family members-do not count.

Can NRIs claim Section 80C if they have no Indian income?

No. Section 80C is a deduction from taxable income. If you have no income sourced in India, there’s nothing to deduct from. You can’t create a tax benefit by investing without taxable income.

Is the principal repayment of a home loan eligible under Section 80C for NRIs?

Yes. The principal portion of your home loan EMI qualifies under Section 80C, whether you're an NRI or resident. You must own the property in India and be making payments from an NRE or NRO account.

Final Tip: Plan Ahead

Section 80C isn’t a last-minute thing. If you wait until March to invest, you might miss out on compounding returns-especially with ELSS or FDs. Start early. Review your investments every January. Keep your bank and tax records updated. And if you're unsure, talk to a tax advisor who understands both Indian tax law and your country’s rules. It’s not expensive, and it could save you far more than the cost of the consultation.