Sector and Thematic Mutual Funds in India: Navigating Concentration Risks and Rewards

Imagine putting all your savings into a single stock. If that company thrives, you win big. If it stumbles, you lose everything. Sector and Thematic Mutual Funds are investment vehicles that focus on specific industries or economic themes rather than the broader market. In India, these funds have gained massive popularity because they offer the chance to ride specific growth waves-like renewable energy, banking, or digital infrastructure-without picking individual stocks.

However, this focused approach comes with a catch. Unlike diversified equity funds that spread risk across hundreds of companies, sectoral funds concentrate your money in a narrow basket. This means higher volatility and sharper drawdowns when that specific sector faces headwinds. For investors in India, understanding the balance between high-reward potential and concentrated risk is crucial before allocating capital to these schemes.

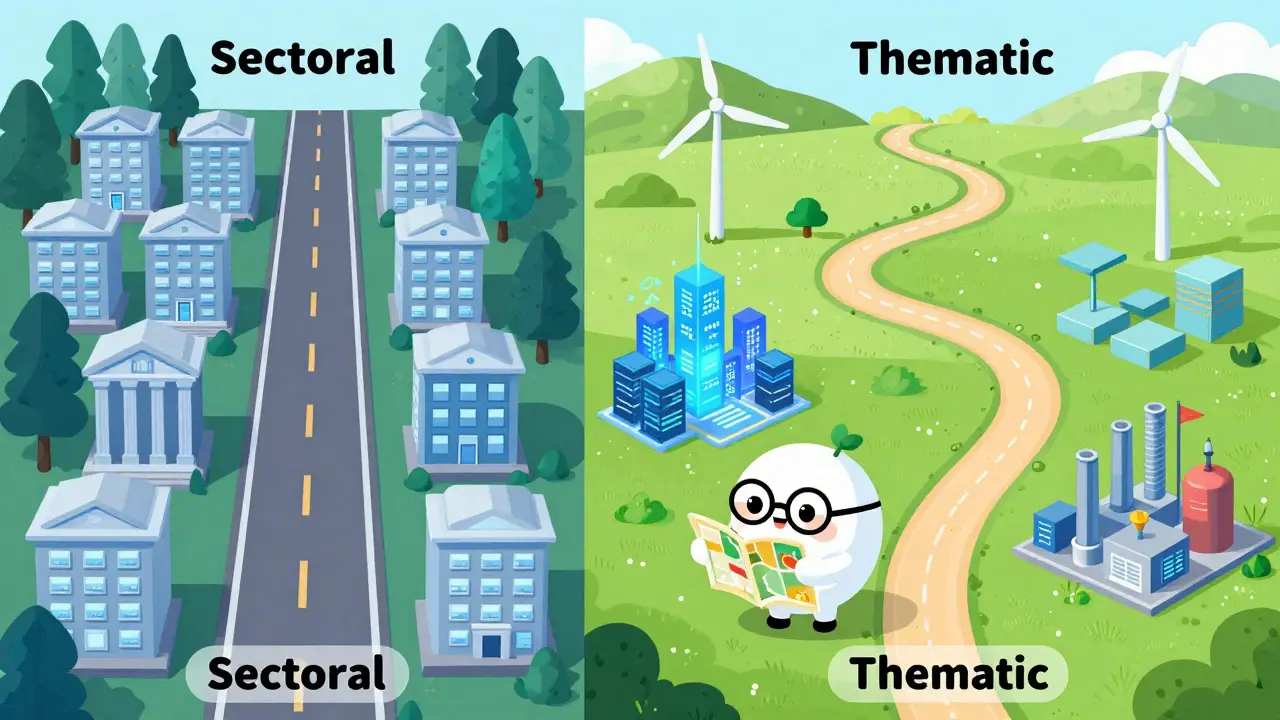

Understanding Sectoral vs. Thematic Funds

To make smart decisions, you first need to distinguish between two similar-sounding categories. While both are concentrated investments, their logic differs significantly.

Sectoral Funds invest in a specific industry or segment of the economy. Examples include Banking & Financial Services, Information Technology (IT), Pharmaceuticals, or Infrastructure. These sectors move together due to common regulatory environments, supply chains, and economic cycles. When the Reserve Bank of India changes interest rates, for instance, the entire banking sector feels the impact simultaneously.

Thematic Funds, on the other hand, invest around a long-term economic theme or trend that may cut across multiple sectors. Think of "Digital India," "Manufacturing Growth," or "Green Energy." A Green Energy fund might hold stocks from solar panel manufacturers (industrial goods), utility companies (power), and electric vehicle makers (automobiles). The unifying factor is the theme, not the industry classification.

| Feature | Sectoral Funds | Thematic Funds |

|---|---|---|

| Focus | Specific Industry (e.g., Pharma) | Economic Trend (e.g., Consumption) |

| Diversification | Low (within one sector) | Moderate (across related sectors) |

| Volatility | Very High | High |

| Market Cycle Dependency | Strongly tied to sector cycle | Tied to structural macro trends |

The Reward Side: Why Investors Love Them

Why do so many Indian investors flock to these funds despite the risks? The answer lies in alpha generation-the ability to outperform the broader market index like the Nifty 50.

When a specific sector is in a bull phase, sectoral funds can deliver returns that dwarf diversified portfolios. For example, during the IT boom of 2023-2024, IT-focused funds delivered double-digit annual returns while the broader market struggled with inflation concerns. Similarly, as India pushes for self-reliance in manufacturing under the "Make in India" initiative, thematic funds focusing on capital goods and defense have seen significant inflows.

These funds also allow retail investors to participate in complex growth stories they might not understand deeply. You don't need to be an engineer to benefit from the rise of semiconductor fabrication plants in India; you just need to identify the right thematic fund. This accessibility has democratized access to high-growth segments of the Indian economy.

The Risk Side: Concentration and Volatility

Here is the hard truth: sectoral and thematic funds are not for the faint-hearted. Their primary characteristic is concentration risk. By limiting exposure to a few stocks or sectors, you eliminate the safety net of diversification.

If the pharmaceutical sector faces global regulatory hurdles, every pharma-heavy fund will drop. There is no offsetting gain from a booming auto sector to cushion the blow. This leads to extreme volatility. It is common for sectoral funds to swing by 10-15% in a matter of weeks. For an investor relying on short-term liquidity, this can be disastrous.

Furthermore, timing is incredibly difficult. Sectors rotate based on economic cycles. What performs well in an expansion phase (like commodities) may lag during a recession. Many investors buy sectoral funds at peak performance, only to sell when the cycle turns, locking in losses. This behavioral trap is more prevalent in thematic funds, where narratives often run hot longer than fundamentals justify.

SEBI Regulations and Classification Changes

In recent years, the Securities and Exchange Board of India (SEBI) has tightened rules to protect investors from excessive speculation. In 2025, SEBI further clarified guidelines for category-wise classification of mutual fund schemes.

Key regulatory constraints include:

- Minimum Investment Requirement: Funds must invest at least 80% of their assets in the specified sector or theme.

- Disclosure Norms: Asset Management Companies (AMCs) must clearly disclose the risks associated with concentration in the Scheme Information Document (SID).

- Expense Ratio Caps: To prevent cost creep, expense ratios for these active strategies are capped relative to benchmark indices.

These regulations ensure transparency but do not eliminate risk. They simply force AMCs to stay true to their mandate, preventing them from drifting into safer, unrelated sectors during downturns.

Who Should Invest? Suitability Check

Not everyone should allocate capital to sectoral or thematic funds. Here is a quick suitability checklist:

- Risk Appetite: You must be comfortable with high volatility and potential temporary losses of 20% or more.

- Investment Horizon: Ideally, you should hold these investments for 5+ years to ride out sectoral cycles.

- Portfolio Allocation: Limit exposure to 10-15% of your total equity portfolio. Never go "all-in" on one theme.

- Knowledge Level: You should have a basic understanding of the sector's drivers (e.g., interest rates for banks, export demand for IT).

If you are a conservative investor nearing retirement, these funds are likely unsuitable. Stick to diversified large-cap or hybrid funds instead.

How to Build a Balanced Portfolio with Thematic Exposure

You can still capture the upside of India's growth story without jeopardizing your financial security. The key is strategic allocation.

Start with a core portfolio of diversified index funds (like Nifty 50 or Nifty Next 50). This forms your stable base. Then, use satellite positions in sectoral/thematic funds to boost returns. For example, if you believe in India's infrastructure push, allocate 5% to an Infrastructure Fund and 5% to a Defense-Themed Fund. Keep the rest in broad market indices.

Regular rebalancing is essential. If your thematic fund surges and now represents 20% of your portfolio, trim some profits and move them back to your core holdings. This disciplined approach ensures you don't get overexposed to a single narrative.

Are sectoral mutual funds tax-efficient in India?

Yes, equity-oriented sectoral funds follow the same tax rules as regular equity funds. Long-term capital gains (LTCG) above ₹1.25 lakh per year are taxed at 10%. Short-term gains are taxed at 20%. Always consult a tax advisor for personalized advice.

What is the minimum investment amount for thematic funds?

Most mutual funds in India allow lump-sum investments starting at ₹500 or even ₹100. Systematic Investment Plans (SIPs) often start at ₹500/month. Check the specific AMC's website for exact figures.

Can I exit a sectoral fund quickly if the market drops?

Technically yes, but it is risky. Selling during a dip locks in losses. Sectoral funds are volatile; exiting prematurely often means missing the eventual recovery. Only exit if the fundamental thesis of the sector has broken.

Which sectoral funds have performed best in the last 5 years?

Historically, IT, Banking, and Pharma funds have shown strong performance during their respective boom cycles. However, past performance does not guarantee future results. Always analyze current valuations before investing.

Is it better to pick individual stocks or use sectoral funds?

For most retail investors, sectoral funds are safer. They provide professional management and reduce single-stock risk within the sector. Picking individual stocks requires deep research and time, which many investors lack.