Direct vs Regular Mutual Funds in India: How Direct Plans Save You Money

Imagine two identical jars. One is labeled "Direct" and the other "Regular." Both contain the same investment strategy, managed by the same fund manager, tracking the same index or portfolio of stocks. Yet, after ten years, one jar holds significantly more money than the other. The difference isn't luck or market timing. It’s a hidden fee structure that silently drains your wealth every single year.

In India, where millions participate in Systematic Investment Plans (SIPs), this distinction between Direct Mutual Funds is mutual fund plans sold directly to investors without intermediaries, offering lower expense ratios and higher net returns and regular plans is not just a technicality-it is the single biggest factor within an investor's control regarding final returns. If you are investing through a broker, an advisor, or even some popular fintech apps that charge for advisory services, you might be paying for a service you didn't explicitly ask for, at the cost of your compounding gains.

The Anatomy of Expense Ratios

To understand why direct plans win, you first need to look at the Expense Ratio is the annual fee charged by a mutual fund to cover operational costs, management fees, and distributor commissions, expressed as a percentage of assets under management. Think of it as the rent you pay to live in the house of your investment. In India, the Securities and Exchange Board of India (SEBI) caps these ratios, but there is still room for variation.

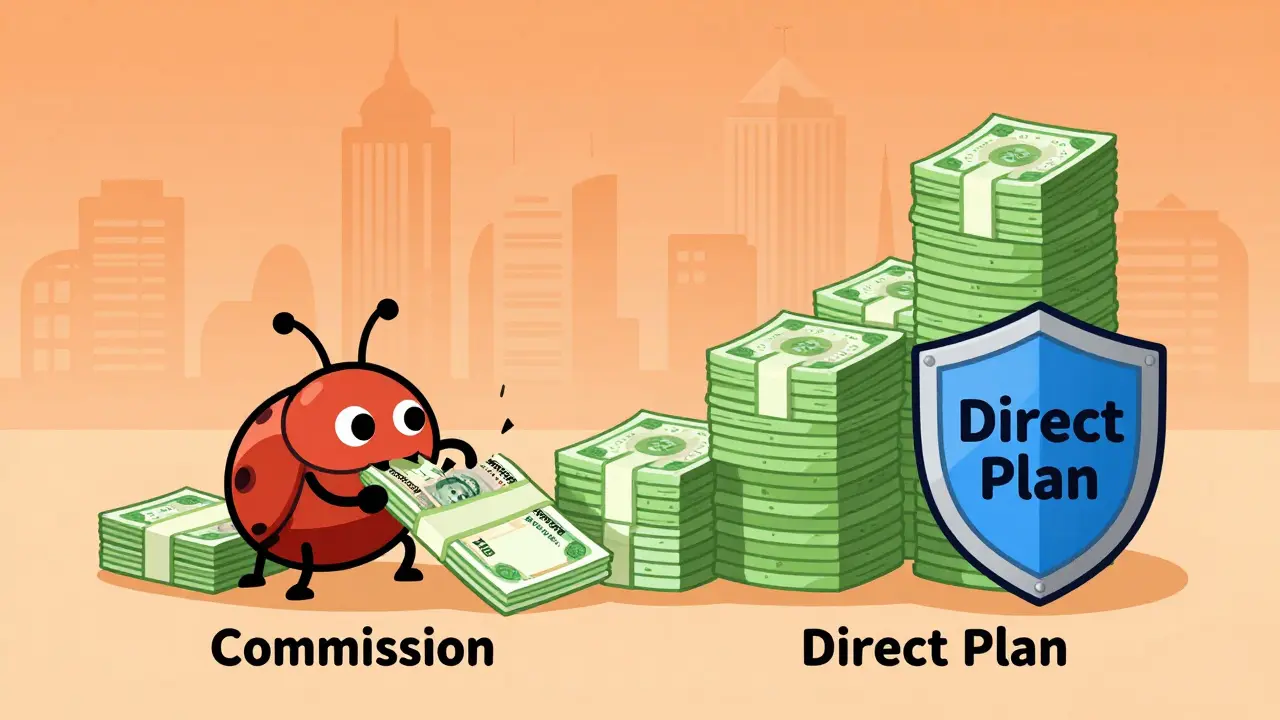

A regular mutual fund plan includes a commission component. When you buy through a distributor-be it a bank branch, a financial advisor, or an online platform-they earn a trail commission. This commission is baked into the expense ratio. For example, if a fund has a gross expense ratio of 1.5%, the distributor might take 0.5% to 1.0% of that. The remaining amount goes toward managing the fund.

In contrast, a direct plan cuts out the middleman. Since there is no distributor earning a trail commission, the entire expense ratio is utilized for fund management and operations. SEBI regulations have made this clearer over the years, requiring Asset Management Companies (AMCs) to disclose these differences transparently. As of recent regulatory updates, the gap between direct and regular expense ratios often hovers around 0.5% to 1.0% annually. That sounds small on paper, but in the world of compounding, small percentages create massive divergences.

The Math Behind the Magic

Let’s strip away the jargon and look at real numbers. Suppose you invest ₹10,000 per month via SIP for 20 years. You choose a diversified equity fund that generates a gross return of 12% before expenses.

| Plan Type | Expense Ratio | Net Annual Return | Final Corpus |

|---|---|---|---|

| Regular Plan | 1.5% | 10.5% | ₹74.8 Lakhs |

| Direct Plan | 0.5% | 11.5% | ₹93.6 Lakhs |

Look at that difference. By choosing the direct plan, you end up with nearly ₹19 lakhs more. You didn’t work harder. You didn’t time the market better. You simply avoided paying for distribution. This extra money is pure profit retained in your pocket because you bypassed the intermediary layer. Over longer horizons, such as 25 or 30 years, this gap widens exponentially due to the power of compounding on the higher net returns.

Who Are the Intermediaries?

Understanding who takes the cut helps you identify where you stand. The ecosystem involves several players:

- Banks and NBFCs: Traditional banks often push regular plans because they earn significant trail commissions. They may present these as "advisory services," but rarely do they provide active portfolio rebalancing for average retail investors.

- Financial Advisors: Certified advisors charge fees or earn commissions. If you pay a flat fee to an advisor, you should ensure you are buying direct plans so you aren't double-paying. If you don't pay a fee, the advisor is likely earning from the regular plan commission.

- Digital Platforms: Many fintech apps offer both options. Some charge a subscription fee for access to direct plans, while others default to regular plans to earn revenue. Always check the "Plan Category" dropdown when purchasing.

The key question is: Are you receiving personalized advice worth the 0.5% to 1.0% annual drag on your returns? For most disciplined long-term investors who follow a simple asset allocation strategy, the answer is no. The cost outweighs the benefit.

How to Identify and Buy Direct Plans

You cannot always tell by looking at the fund name alone. A fund named "HDFC Top 100 Fund" exists in both Direct and Regular categories. Here is how to spot the difference:

- Check the ISIN Code: Every mutual fund scheme has a unique International Securities Identification Number (ISIN). Direct and Regular plans have different ISIN codes. Look for the suffix "D" for Direct and "R" for Regular in the code or plan description.

- Read the Scheme Name Carefully: On platforms like Groww, Zerodha Coin, or AMC websites, the plan type is usually listed next to the fund name. It will explicitly say "Direct Growth" or "Regular Growth."

- Compare NAVs: The Net Asset Value (NAV) of direct plans is always higher than regular plans for the same fund. This is because direct plans have deducted fewer fees over time. If you see two NAVs for the same fund, the higher one is almost certainly the direct plan.

Buying direct is straightforward. You can invest directly through the Asset Management Company’s website, though this can be cumbersome if you hold funds across multiple AMCs. Alternatively, use discount brokers or robo-advisors that specialize in direct-only offerings. These platforms make it easy to consolidate your holdings and track performance without hidden commissions.

When Might Regular Plans Make Sense?

Fairness demands we acknowledge scenarios where regular plans might justify their cost. If you are completely new to investing, lack the discipline to research funds, and need someone to guide you through market volatility, a trusted financial advisor can add value. However, this only makes sense if:

- The advisor charges a transparent, flat fee rather than relying solely on trail commissions.

- You receive regular reviews, tax-loss harvesting, and asset allocation adjustments.

- You are investing large sums where behavioral coaching prevents panic selling during crashes.

For the vast majority of Indian retail investors using SIPs for retirement or child education goals, the self-directed approach via direct plans is superior. The information asymmetry has decreased dramatically thanks to internet resources, making professional intermediaries less necessary for basic fund selection.

Tax Implications and Exit Loads

It is crucial to note that tax treatment remains identical for both direct and regular plans. Short-term capital gains (STCG) on equity funds held for less than one year are taxed at 20%. Long-term capital gains (LTCG) above ₹1.25 lakh per year are taxed at 12.5%. There is no tax advantage to either plan type.

Similarly, exit loads-the penalty for withdrawing money early-are the same for both. Most equity funds charge 1% if you redeem within a year. So, switching from regular to direct later doesn't save you exit load costs; you lose the accumulated drag from the higher expense ratio during the holding period. Always start with direct to maximize efficiency from day one.

Can I switch my existing Regular Mutual Fund to Direct?

Yes, you can switch, but it is treated as a redemption followed by a fresh purchase. This triggers capital gains tax if the fund is profitable. You also incur exit loads if you redeem within the specified lock-in period (usually one year). To avoid taxes, consider starting new SIPs in direct plans and letting old regular investments mature naturally.

Are Direct Plans Riskier Than Regular Plans?

No. The underlying portfolio, fund manager, and risk profile are identical. The only difference is the fee structure. Direct plans do not expose you to additional market risk; they simply return more of the generated profit to you.

Do all Mutual Funds in India offer Direct Plans?

Yes, SEBI mandates that all open-ended equity and debt schemes must offer direct plans. However, some closed-ended schemes or specific institutional plans may vary. Always check the scheme factsheet to confirm availability.

Is it hard to manage Direct Plans myself?

Not necessarily. With modern digital platforms, setting up auto-debits and tracking performance is automated. You only need to decide which funds to buy initially and periodically rebalance your asset allocation. For passive index fund investors, the effort is minimal.

What is the typical expense ratio difference in 2026?

As of 2026, the average difference between direct and regular expense ratios for active equity funds is approximately 0.5% to 0.75%. For index funds, the gap is smaller, often around 0.1% to 0.2%, since index funds already have low base costs.